Best Credit Card in India (2026): Find the Right One for Your Spending Profile

Last updated on

Find the best credit card in India for your salary, spending habits, and life stage. Covers students, salaried professionals, HNIs, travellers, and cashback maximisers, with real earn-rate math and hidden condition warnings.

Too busy to read endless reviews & research?

Find the best cards that suit your lifestyle in 30 seconds

Try Monzy NowNo signup or email required

You know that colleague at your office who swears by his HDFC Regalia Gold? He's been raving about it for two years. But ask him how many reward points he's actually redeemed, and watch the silence. Or that friend who "upgraded" to a ₹12,500-fee card last year because it came in metal only to realise six months later that his lounge access now requires spending ₹50,000 in the previous quarter.

Welcome to Indian credit cards in 2026: powerful, complex, and full of traps that weren't there three years ago.

Every listicle claiming to name the best credit card in India is designed to manipulate your thought by omission.

In fact, the best card is entirely a function of your spending habits: your day to day spend categories, monthly spends, your fee tolerance, your city, your lifestyle.

A card that makes perfect sense for a frequent flyer in Delhi is a waste of plastic for a Tier-2 city resident who shops locally and fills up fuel twice a week.

Comparing credit cards without knowing your own numbers first is the most common mistake most people make in India.

Thankfully, I learnt it the hard way after wasting hours on approximately 25+ applications and reading through 10000 threads in the past 1 year. So, I thought of making this guide where I present to you a simple yet effective way to pick a credit card that works the best for yourself.

No matter if you're picking your first card, upgrading from an entry-level one, or rebuilding your wallet after a round of devaluations, this is the framework to make the right call.

Why Old Credit Card Advice No Longer Works?

Between 2023 and 2025, virtually every major issuer in India quietly rewrote the rules of the reward game. HDFC Bank slashed the accelerated earn rates on SmartBuy. SBI Card announced a significant devaluation of the SBI Cashback Card effective April 2026, reducing its headline cashback rate on online spends. Axis Bank overhauled Magnus and Atlas benefits. The era of flat, uncapped reward rates on all transactions is effectively over.

Three structural changes define the 2026 landscape:

1. Spend-based milestone gates have replaced flat rewards. Cards that once earned 5% on all online spends now earn 1.5% baseline, with the higher rate unlocked only after you hit ₹1.5–₹2L in a quarter. This benefits high spenders but actively punishes moderate spenders who used to rely on these cards for everyday returns. Milestone benefits, like bonus rewards, vouchers, or complimentary airport lounge access triggered at specific annual spend thresholds, have similarly been restructured upward, requiring higher spend to unlock the same perks that used to be baseline.

2. Welcome benefits and renewal benefits have become conditional. The days of showing your card at the IndiGo lounge in Bengaluru without any strings attached are largely gone. Most cards, including the Axis ACE and the HDFC Millennia, now require a minimum spend of ₹50,000 (and even more) in the preceding three calendar months to unlock complimentary lounge visits.

Welcome benefits like vouchers and bonus rewards points are typically gated behind a minimum spend in the first 60–90 days. Renewal benefits follow the same pattern: miss the annual spend threshold, and you lose both the fee waiver and the renewal perk in a single blow.

3. Reward point values have fractured. HDFC's Infinia earns 5 reward points per ₹150, but 1 point equals ₹0.50 only when redeemed for flights or hotels via SmartBuy, and even then, the redemption is capped at 70% of booking value, requiring mandatory co-payment. The advertised 33.33% reward rate on Infinia is, in practice, available only to a tiny fraction of users who understand the redemption mechanics.

So, I see a pattern here: the old advice of getting the card with the highest reward rate no longer works. Now, you need to ask: what is my primary spend category, at what volume, and how good am I at optimising redemptions?

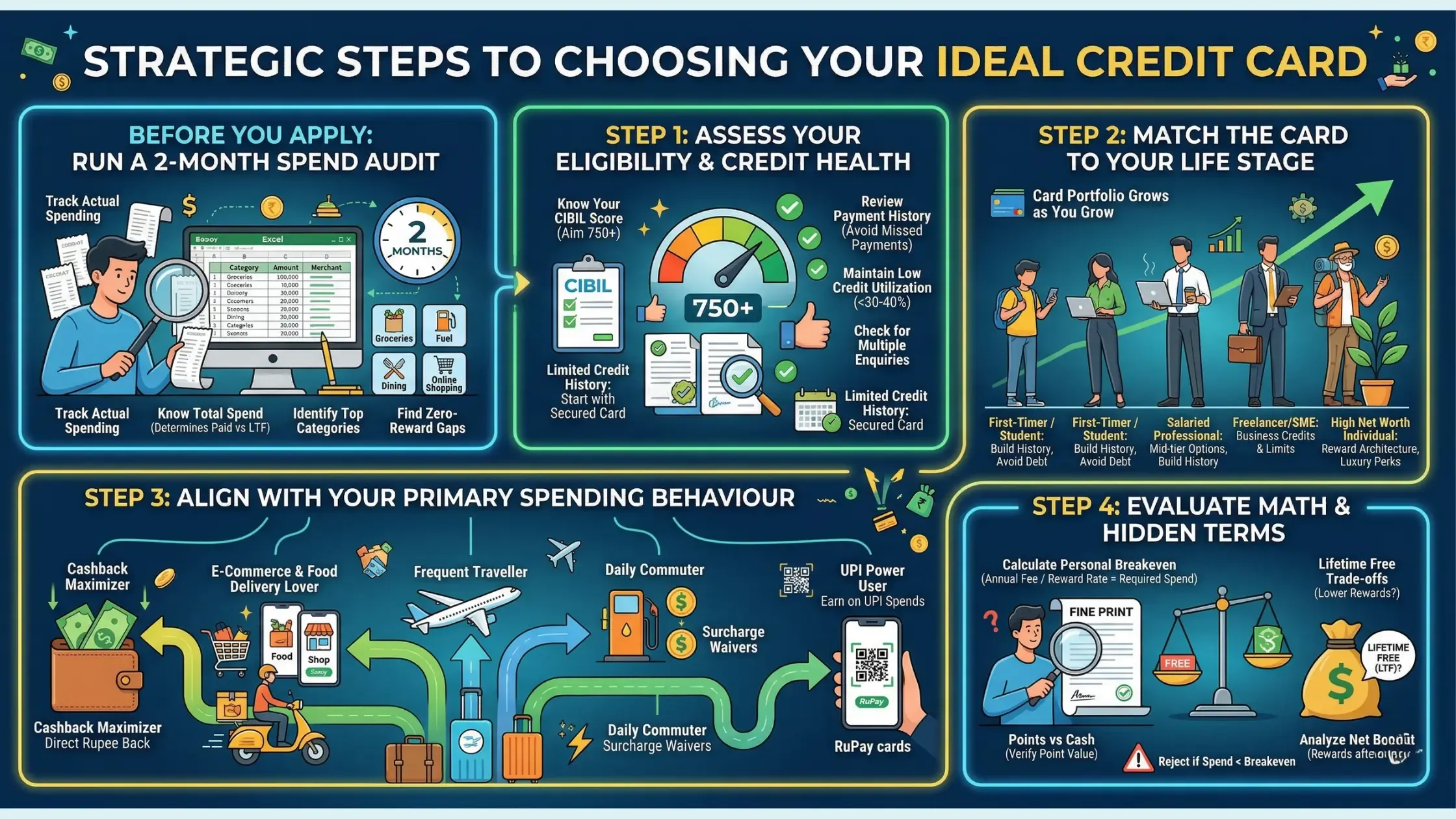

Before You Apply: Run a 2-Month Spend Audit

I have talked to many people who pick a credit card the same way they pick a restaurant on Zomato: scroll, look at the rating, order. The problem is that a 4.2-star card for someone in Mumbai with a ₹1.5L salary and heavy Amazon spend is a terrible card for someone in Nagpur spending mostly on fuel and local groceries.

So, what should we do if not look at the ratings and review on top platforms offering best credit card india lists?

The most methodical approach I could frame out is to track your actual spending for two months before applying for anything. An Excel sheet with columns for category, amount, and merchant is enough. After two months, you'll know:

- Your total monthly spend (determines LTF vs. paid card viability).

- Your top 2–3 spend categories by volume (determines which card earns best for you).

- Which categories currently earn you zero rewards (the gaps your new card should fill)

This matters because the answer to "should I get a paid card or LTF?" is entirely a function of your spend volume and category mix, not the card's star rating on some website.

A ₹500/year paid card that earns 3% on your ₹8,000/month grocery spend returns ₹2,880/year. An LTF card that earns 1% on the same spend returns ₹960/year. The paid card wins by ₹1,880 after fee. But if your grocery spend is ₹2,000/month, the math flips.

Do the audit first. Then move on to the next steps.

Step 1: Assess Your Eligibility & Credit Health

Before comparing reward rates, you need to know whether you'll actually get approved for the card you want.

Know Your CIBIL Score

A CIBIL score of 750 or above is the standard threshold for premium and mid-tier credit cards in India. HDFC, Axis, ICICI, and SBI Card all run automated eligibility filters.

Below 750, you're routed to secured cards or entry-level credit cards.

Below 700, some issuers will decline outright.

Just a reminder that your CIBIL score is a composite of payment history (35%), credit utilisation (30%), credit age (15%), credit mix (10%), and new enquiries (10%).

The most common score-killers among Indian cardholders: missed EMI payments even once, credit utilisation above 40%, and multiple hard enquiries from applying to too many cards in a short window.

If you have a limited credit history, say you're a a recent graduate or someone who has only ever used a bank account with no loans or cards, your CIBIL score may simply be absent rather than low, which puts you in the same bracket as a secured card applicant regardless of income.

Remember building a good credit score takes 12–18 months of responsible card usage: full payments before the due date, utilisation below 30%, and no missed payments. There are no shortcuts.

Once you've had the card for 9–12 months with clean payments, you can request a credit limit increase. Most issuers approve 25–30% bumps for cardholders in good standing.

Step 2: Match the Card to Your Life Stage

One of the most honest pieces of credit card advice you'll find online about picking the right card is that you should not try to optimise too early.

I talked to an experienced credit card user who described their own journey as starting with HDFC Millennia, swiping it without overthinking it, getting upgraded to Regalia Gold through consistent spend, and only then, after years of building a natural card history, entering the miles and points game intentionally. The full strategy only crystallised after the lifestyle organically called for it.

This is advice no credit card tool or Top 10 listicle will give you, because it's not monetisable. But it's real: your card portfolio should grow as you grow. Trying to jump to a ₹12,500/year card at 24 on a ₹40,000 salary because it looks impressive is how people end up trapped by annual fees they can't justify.

Match the card to where you actually are, not where you aspire to be.

As a First-Timer or Student

If you're under 25, in college, or just started your first job below ₹25,000/month, your only goal with a credit card is to build credit history without paying annual fees or accumulating debt. Not to maximise rewards. Not to get lounge access. Just to establish a clean repayment track record.

Entry-level cards are purpose-built for this. Three worth knowing:

- Amazon Pay ICICI (₹0/year): 5% cashback on Amazon.in for Prime members, 1% on everything else, no redemption required, cashback credits directly to your Amazon Pay balance. No income proof needed if you have an existing ICICI savings account.

- IDFC FIRST WOW (₹0/year): Issued against a Fixed Deposit, so approval is almost guaranteed regardless of income or CIBIL history. Zero forex markup, 4 complimentary domestic lounge visits annually — unusual for a ₹0-fee card. Best first card if you have no credit history at all.

- Axis Neo (₹250/year): Low fee, 10% cashback on Zomato and Swiggy (capped ₹50/month per platform), 1% on all other spends. Works for a student who orders food regularly and wants their first non-FD-backed card.

The golden rule at this stage: pay the full statement balance every month, not just the minimum. One month of carrying a ₹10,000 balance at 40% APR wipes out six months of cashback.

Best credit cards for students and first-timers in India →

As a Salaried Professional

₹30,000–₹1L/month is the most competitive income bracket for credit card issuers. Every bank wants this customer, which means the card options here are genuinely good, but also genuinely confusing.

Three cards that consistently earn their keep at this income level:

- Axis Bank ACE (₹499/year): 5% cashback on Swiggy, Zomato, and Ola via Google Pay (capped ₹500/month combined), 1.5% on all other spends. The 1.5% flat rate is the real feature — it's unconditional. Fee waiver at ₹2L annual spend. At ₹25,000/month total spend, this card returns roughly ₹3,700–₹4,500/year after fee.

- HDFC Millennia (₹1,000/year): 5% cashback on Amazon, Flipkart, Swiggy, Zomato, Myntra, BookMyShow (capped ₹1,000/month across all), 1% on offline and other online spends. Fee waiver at ₹1L/quarter (₹4L/year). Best if your spend is concentrated on these specific platforms.

- HDFC Regalia Gold (₹2,500/year): 4 reward points per ₹150 (general rate ~1.33%), accelerated 5x on select SmartBuy partners. 4 domestic lounge visits/quarter + 2 international via Priority Pass. Fee waiver at ₹4L/year. The right upgrade once you're consistently spending ₹35,000+/month and want lounge access.

The issuer ladder matters here.

HDFC's internal credit progression runs Freedom → Millennia → Regalia Gold → Regalia → Infinia. Applying for Regalia Gold before holding Millennia for 12+ months often results in rejection.

The upgrade trap: Many professionals hold an entry-level card for 2–3 years, hit a salary hike, and apply for a premium card without assessing whether their spend volume justifies the higher annual fee. A ₹2,500/year card like HDFC Regalia Gold requires ₹4L annual spend for fee waiver. If you're spending less than that, your rewards will not cover the fee.

Best credit cards for salaried professionals →

Freelancers, SMEs & Business Owners

If your monthly business expenses cross ₹2L: GST payments, vendor bills, subscription tools, travel, a personal credit card is the wrong instrument. Business credit cards issue GST-compliant invoices on annual fees, offer higher credit limits, and can separate personal and business spend cleanly.

The practical friction: most Indian issuers underwrite business cards on ITR income. If your declared income is ₹5L/year but actual cashflow is ₹30L/year, you'll be offered limits that don't match your actual needs.

For proprietors and consultants with clean ITR filings, the SBI Card PRIME (₹2,999/year) and SBI Card ELITE (₹4,999/year) are worth examining: both have higher spend-linked milestone rewards than most entry business cards, and SBI's underwriting criteria is often more flexible for salaried-equivalent freelancers.

For high GST-volume operators, some issuers' like HDFC offer specialized cards like HDFC Biz Black with great offers and rebates specifically on GST payment transactions.

Best credit cards for business owners and freelancers

High Net Worth Individuals (HNIs)

At ₹12,500/year and above, the card fee is irrelevant. What matters is whether the reward architecture genuinely works for how you actually spend.

- HDFC Infinia Metal (₹12,500/year): 5 reward points per ₹150 spent, each point worth ₹0.50 when redeemed for flights/hotels via SmartBuy — giving a ~1.67% general rate, or up to 3.33% on 5x SmartBuy categories. Complimentary Club Marriott membership (worth ₹5,000–₹8,000/year standalone), unlimited domestic lounge access. The headline 33.33% SmartBuy rate exists but requires booking entirely through the portal at up to 70% of booking value — it's real, but accessible only to users who understand the mechanics.

- HDFC Regalia Gold (₹2,500/year): Often the smarter starting point before Infinia — 4 pts per ₹150 (~1.33% general), 5x on SmartBuy partners (~3.33%), 4 domestic lounge visits/quarter + Priority Pass. At ₹4L annual spend, fee is waived entirely.

- Axis Atlas (₹5,000/year): 2 EDGE Miles per ₹100 (~2% general), up to 5% on travel portal bookings. Best-in-class for frequent flyers who book through the portal. Fee waiver at ₹7.5L annual spend.

The honest test for any premium card: take your actual annual spend in the card's highest-earning category, multiply by the accelerated rate, subtract the annual fee. If the net is positive, the card works. If not, it doesn't matter how prestigious it looks.

Best premium credit cards for HNIs →

Step 3: Align with Your Primary Spending Behaviour

This is the section most people skip and most people regret skipping after a few years. Basically, you should try to map your card needs to your actual spends (as I shared above).

Once you know your regular spending habits, you can pick cards based on your spending preferences. Here, you have 3-4 options, based on your own behavior:

If you're a Cashback Maximiser

You want rupees back in your account, not points in a loyalty wallet you'll forget about.

The key differentiator is how the cashback is credited: some cards credit directly to your statement balance (Axis ACE: 1.5% on all spends, 5% on Google Pay utilities/Swiggy/Zomato/Ola — capped at ₹500/month combined), while others credit to platform wallets.

You should also understand an important distinction between a cashback credit card and a rewards credit card here.

A Cashback card give you a direct rupee value as statement credit or wallet balance with no conversion rate ambiguity.

Rewards credit cards give you points that must be redeemed through a catalogue or portal, and the effective rupee value per point depends entirely on how and where you redeem.

For most people who want to save money without optimisation overhead, the best credit cards are actually the ones with the simplest cashback mechanics: earn directly, credit automatically, spend freely.

The Amazon Pay ICICI remains the strongest LTF cashback cards in India: 5% uncapped on Amazon.in, 2% on Amazon Pay partner merchants, 1% everywhere else.

Cashback credits directly to your Amazon Pay balance, essentially spendable cash. No redemption fees. No minimum balance. If you frequently shop online and Amazon is your primary platform, this card earns bonus rewards passively every time you shop.

For the SBI Cashback Card, which was the dominant online cashback card until April 2026, the recent devaluation has changed the benefits significantly. Always check the current rate structure before applying. Here's more about SBI Cashback Credit Card Devaluation

If You're an E-Commerce & Food Delivery Lover

If your monthly credit card statement reads like a Swiggy/Zomato/Amazon/Flipkart scroll, co-branded cards are purpose-built for you.

- Amazon Pay ICICI (₹0/year): 5% on Amazon for Prime members, 2% on Amazon Pay partners. Best LTF cashback for Amazon loyalists. Also earns when you pay bills and recharges via Amazon Pay.

- Flipkart Axis Bank Card (₹500/year): 5% on Flipkart and Myntra (uncapped), 4% on preferred partners, 1.5% everywhere else. Annual fee waiver requires ₹3.5L annual spend.

- Swiggy HDFC BLCK Credit Card (₹500/year): 10% cashback on all Swiggy spends. Zero lounge access.

One underrated benefit across multiple co-branded and mid-tier cards is the movie ticket discount. Cards like HDFC Millennia, SBI Card PRIME, and Axis ACE offer discounts of ₹100–₹250 per movie ticket booking via BookMyShow or Paytm Movies, typically limited to 2 transactions per month.

On a ₹300 ticket, that's a 33–83% saving, a key benefit that doesn't show up in the headline reward rate but adds up to ₹2,400–₹6,000/year for regular cinema-goers.

Similarly, many of these cards offer additional travel benefits like accelerated rewards on cab bookings (Ola, Uber) and train tickets, complementing their core use case of shopping online.

The catch with co-branded cards: ecosystem lock-in. The Swiggy HDFC card might earn nothing on Zomato and vice versa.

If you're a Frequent Traveller

For 4+ domestic trips and 1–2 international trips per year, the card math shifts entirely. Rewards on grocery and food delivery become secondary. What you actually need is unconditional lounge access, a forex markup below 2%, and a reward structure that pays you back on the flight and hotel spend you're already making.

The catch in 2026: lounge access has become the most quietly conditional benefit in Indian credit cards. Most mid-tier cards now require ₹50,000 in spend during the previous quarter to unlock your "complimentary" visits. That's not complimentary — that's a spend gate. Before assuming any card gives you lounge access, check whether last quarter's spend clears the threshold.

Card | Dom. lounge | Intl. lounge | Spend gate | Forex markup | Annual fee |

|---|---|---|---|---|---|

Axis Atlas | 18/year | 12/year | Tier-based (₹3L annual for Gold) | 3.5% | ₹5,000 |

HDFC Regalia Gold | 12/year (4/quarter) | 6/year via Priority Pass | None (verify current T&Cs) | 2% | ₹2,500 |

ICICI Sapphiro | 4/quarter | 2/quarter via Dreamfolks | ₹5,000 prev. quarter | 3.5% | ₹3,500 |

One thing worth knowing before booking a lounge visit on any card: Indian airports have been tightening guest policies and restricting which lounges honour specific card networks. Always cross-check your card's current lounge list before travel: ICICI publishes a specific Sapphiro lounge access list that's worth bookmarking if you go that route.

For a deeper dive on how these three cards compare across actual flight-booking scenarios and miles redemption strategies, see the full guide to best credit cards for travel in India.

If You're a Daily Commuter...

Fuel credit cards in India are fundamentally about one thing: the 1% fuel surcharge waiver that petrol pumps levy on all credit card transactions. On a ₹5,000/month fuel spend, that's ₹50/month or ₹600/year.

Most "fuel cards" claim to earn reward points on fuel purchases. But in reality: HDFC, Axis, SBI, and ICICI all explicitly exclude fuel from reward point accrual as of 2025–26. Fuel earns zero reward points on HDFC Regalia Gold, Axis Magnus, and most premium cards. The surcharge waiver is the real benefit, not the points.

But some co-branded cards can deliver meaningful fuel savings, well above what a general-purpose card earns on the same fuel purchases. For a full analysis of which cards actually deliver fuel value, see best fuel credit cards with surcharge waivers in India.

For The UPI Power Users

If you're paying for groceries at DMart, morning chai at a local stall, auto rides, and electricity bills all via UPI on a debit card, you're leaving money on the table every single day.

RuPay credit cards linked to UPI change this entirely. The Kiwi RuPay credit card is specifically optimised for UPI reward earning on everyday small-ticket spends. The HDFC Bank UPI RuPay Credit Card (₹99/year) also earns up to 3% cashback on groceries, dining, and utility bill payments made via UPI. The Kotak UPI RuPay Credit Card (₹0/year) earns 0.75% on all UPI spends with no per-category restriction.

The key limitation: UPI reward rates on RuPay credit cards are typically capped at low monthly limits. But even capped, earning 2–3% on small-ticket UPI spends is a meaningful upgrade from earning zero on a debit card.

Your top spend | Best card type | Cards to consider |

|---|---|---|

Online shopping | Flat cashback | HDFC Millennia (5% on Amazon/Flipkart, ₹1,000/yr), Axis ACE (1.5% everywhere, ₹499/yr) |

Food delivery | Co-branded cashback | Swiggy HDFC Bank Card (10% on Swiggy, ₹500/yr), Axis ACE (5% via Google Pay) |

Flights & hotels | Miles / travel rewards | Axis Atlas (2 EDGE miles/₹100, ₹5,000/yr), HDFC Regalia Gold (Priority Pass, ₹2,500/yr) |

Fuel | Surcharge waiver + fuel rewards | BPCL SBI Octane (6.25% best-case on BPCL, ₹1,499/yr), fuel card comparison → |

Groceries & utilities | UPI/RuPay cashback | HDFC UPI RuPay (up to 3% on UPI grocery/utility, ₹99/yr), Kiwi RuPay |

All-round / HNI | Premium rewards | HDFC Infinia Metal (3.33% general, 33.33% SmartBuy cap, ₹12,500/yr) |

Note: "best-case" rates apply only in specific redemption scenarios. The general rate is what you'll earn in everyday use — always calculate ROI on the general rate.

Step 4: Evaluate the Math & Hidden Terms

The Reality of Lifetime Free (LTF) Cards

"Lifetime Free" sounds like the obvious choice. No annual fee, no fee waiver stress, no renewal anxiety. A lifetime free card also eliminates the risk that comes with holding multiple credit cards where some have fee deadlines you might miss.

But LTF cards come with a structural problem: issuers have no recurring fee revenue to fund premium reward rates, concierge credit card services, or lounge tie-ups. So, as a result, a lot of LTF cards offer effective reward rates of 0.5–1.5%, far below the 3–5% available from mid-tier paid cards.

The Amazon Pay ICICI is the notable exception: 5% LTF cashback on Amazon Prime purchases is genuinely excellent for a zero-fee card. Kiwi Credit card is also good. But outside these specific use cases, a ₹500–₹1,000/year paid card with a 3–5% reward rate on your primary spend category might be a better option.

Let's take an example.

Axis ACE costs ₹499/year. At 5% cashback on Swiggy/Zomato/Ola (capped ₹500/month combined) and 1.5% on everything else, a user spending ₹20,000/month earns roughly ₹300–₹400/month in rewards, ₹3,600–₹4,800/year. After the ₹499 fee, net benefit is ₹3,100–₹4,300.

For a detailed analysis of when LTF is genuinely better and when it's a trap, see the truth about lifetime free credit cards in India.

Calculating the True Reward Value

This is where most cardholders get misled. "5 reward points per ₹100 spent" is meaningless without knowing what 1 reward point is worth in actual rupees at redemption.

Before that table though, here's a framework that cuts through all the noise. You can create a personal ROI calculator, applied category by category:

- Identify a spend category currently earning you zero rewards (fuel, internet bill, flight bookings, groceries)

- Search for the best cards in that specific category, based on research, not "top 10 cards overall"

- Calculate your personal breakeven: annual fee ÷ reward rate = spend required to recover the fee

- Compare that breakeven spend to your actual annual spend in that categoryIf your real spend exceeds the breakeven → get the card. If not → reject it, regardless of how good it looks on paper

For example, Axis Atlas at ₹5,000/year with ~10% on flight bookings requires ₹50,000 in annual flight spend just to break even.

If your actual annual flight spend is ₹50,000, you're not making money, you're recovering the fee. The card only becomes financially positive above that threshold. Most people applying for travel cards are not clearing it.

Applied to fuel savings, SBI BPCL Octane at ₹1,500/year with ~6.25% returns on fuel requires approximately ₹24,000 in annual fuel spend (₹2,000/month) to break even.

If you're driving a diesel SUV and spending ₹5,000+/month on fuel, the card makes clear sense. If you're a light commuter spending ₹2,000/month, you're at exactly breakeven, the card earns you nothing net.

This is the calculation to run before every card application.

Card | Earn Rate | Point Value | Effective Return |

HDFC Infinia Metal | 5 pts per ₹150 | ₹0.50/pt (SmartBuy travel) | ~1.67% baseline; capped at 70% of booking value |

HDFC Regalia Gold | 4 pts per ₹150 | ₹0.50/pt | ~1.33% general; ~3.33% on 5x partners |

Axis Magnus | 12 pts per ₹200 | ~₹0.20/pt (EDGE Rewards) | ~1.2% base; ~6% general; ~30% on Travel EDGE portal |

Axis ACE | Direct cashback | ₹1 = ₹1 | 1.5% general; 5% on select merchants (capped ₹500/month) |

Amazon Pay ICICI | Direct cashback | ₹1 = ₹1 | 5% on Amazon Prime; 2% partners; 1% others |

YES MARQUEE | YES Rewardz Points | Variable | ~2.25% general; up to 4.5% online |

Remember, cashback cards (Axis ACE, Amazon Pay ICICI) offer transparent, instant value. Points-based cards (HDFC Infinia, Axis Magnus, Axis Atlas) can offer higher effective returns, but only if you actively understand the redemption catalogue, transfer partners, and portal mechanics.

For most users who won't optimise redemptions, a 1.5–2% cashback card out-earns a 5% points card that effectively delivers 1.2% at redemption.

A Solid Strategy for the Perfect Credit Card Wallet in 2026

The optimal credit card setup for most Indians in 2026 is exactly two cards. Not five. Not one. Two.

Card 1: A flat-rate cashback card for everyday spend. This covers your default purchases: groceries, utilities, bill payments, petrol, miscellaneous retail.A card with 1–2% flat cashback on all spends (no category restrictions, no redemption complexity) means you're always earning something without thinking about it. Best options: Axis ACE (1.5% base + 5% on Google Pay/Swiggy/Zomato/Ola, capped), Amazon Pay ICICI (1% base + 5% on Amazon), HDFC Millennia (1% base + 5% on partner merchants, capped at ₹1,000/month).

Card 2: A specialist co-branded or category card for your highest-spend bucket.If your biggest monthly expense is Amazon → the Amazon Pay ICICI doubles as both Card 1 and Card 2. If it's Swiggy/Zomato → pair the Swiggy HDFC card with a general cashback card. If it's travel → Axis Atlas or HDFC Regalia Gold for flights and hotels, paired with Axis ACE for everyday spends.

Why concentration wins over diversification?Spreading spend across five cards dilutes your average monthly spend per card. If a card requires ₹2L annual spend for fee waiver and you split ₹3L/year across four cards, none of them crosses the waiver threshold.

Two cards also means two statement dates to track, not five, which meaningfully reduces the chance of a missed payment and the late payment fees that follow.

When you hold multiple credit cards, the operational overhead grows faster than the reward benefit in most cases.

Every additional card beyond two should clear a simple test: "Does this card earn meaningfully more on a specific category I spend heavily on, and does that incremental return justify the fee and complexity?" Most of the time, the honest answer is no.

Avoiding the Minimum Amount Due Trap

This is the most important financial literacy information in this guide, and it gets the least attention in card marketing materials (or even in online forums).

Your credit card statement shows two numbers: "Total Amount Due" and "Minimum Amount Due." The minimum is typically 5% of the total or ₹200, whichever is higher. Banks present this as a helpful feature: you don't have to pay the full bill right now.

Here's what they don't say clearly: if you pay only the minimum, the remaining balance attracts interest at 36–48% APR (3–4% per month). On a ₹30,000 outstanding balance, that's ₹900–₹1,200 in interest per month, compounding daily. Within a year, you can owe significantly more than you originally spent.

A ₹5,000 reward earned in a year on 2% cashback is completely wiped out by a single month of carrying a ₹25,000 balance at 40% APR. The rewards game only makes financial sense if you are a full-payment user.

If you regularly carry a balance, the interest cost dwarfs any rewards benefit, and the right financial tool is not a rewards card but a 0% EMI product or a personal loan at a lower rate.

Rule: of thumb Never use a credit card for a purchase you cannot pay off in full by the due date.

Frequently Asked Questions

Which is the best credit card in India in 2026?

There is no single best credit card. The right answer depends entirely on your monthly spend volume and which categories you spend most in. For everyday cashback with no complexity, the Axis ACE (₹499/year, 1.5% on everything, 5% on Google Pay/Swiggy/Zomato) is a good card. For online shopping, the Amazon Pay ICICI is the strongest lifetime-free option at 5% on Amazon for Prime members. For frequent travellers taking 4+ flights a year, HDFC Regalia Gold at ₹2,500/year pays for itself through lounge access alone. If you're confused about the best credit card, try Monzy.co to find the card that's best for youin 30 seconds.

How do I choose a credit card based on my salary in India?

Your salary determines which cards you can actually get approved for, not which one is theoretically best. Under ₹15,000/month: secured cards issued against a fixed deposit (IDFC FIRST WOW!, ₹0/year) are the most reliable route. Between ₹20,000–₹30,000/month: unsecured entry cards like Axis ACE and HDFC Millennia become accessible. Between ₹30,000–₹50,000/month: mid-premium cards like HDFC Regalia Gold and ICICI Sapphiro open up. Above ₹1 lakh/month: super-premium cards like Axis Magnus and HDFC Diners Club Black become viable. For a full salary-tier breakdown with specific card picks at each income level, see the guide to best credit cards by salary in India.

What is the best credit card for airport lounge access in India?

For domestic lounge access specifically, HDFC Regalia Gold gives 12 visits per year (4 per quarter) at ₹2,500 annual fee, among the best value in its tier. For unlimited domestic and international lounge access, Axis Magnus at ₹12,500/year covers both with guest privileges. For a mid-fee option with both domestic and international coverage, ICICI Sapphiro provides access via Dreamfolks at ₹3,500/year, conditional on ₹5,000 spend in the previous quarter. One thing to check before relying on any card for lounge access: most cards in 2026 have introduced spend gates, you need to clear a minimum spend in the prior quarter to unlock visits. The Axis Atlas also gives 18 domestic and 12 international visits per year across its tier structure, making it the strongest lounge card if travel spend is already high.

Which credit card gives the best cashback in India?

For direct statement cashback with no redemption complexity, the Axis ACE is the strongest general option: 1.5% on all spends unconditionally, 5% on Swiggy, Zomato, and Ola via Google Pay (capped ₹500/month combined), at ₹499/year. For Amazon-heavy spenders, the Amazon Pay ICICI is lifetime free with 5% uncapped cashback on Amazon for Prime members — the best cashback rate on a zero-fee card in India. For Flipkart loyalists, the Flipkart Axis Bank Card earns 5% on Flipkart and Myntra with 4% on Swiggy and Uber. The key distinction to understand: cashback cards credit rupee value directly (Axis ACE, Amazon Pay ICICI), while rewards cards give points that must be redeemed through a portal at variable rates. For most people who won't actively optimise redemptions, a 1.5% cashback card consistently outperforms a 5% points card that delivers 1.2% at actual redemption.

What is the best first credit card in India?

If you have no credit history at all: the IDFC FIRST WOW! is the standout choice — lifetime free, issued against a fixed deposit, near-guaranteed approval regardless of income or CIBIL score, with 4 free domestic lounge visits and zero forex markup. If you have a CIBIL score above 700 and a salary of ₹20,000+: the Axis ACE or Amazon Pay ICICI are the best first unsecured cards, both have straightforward cashback structures that reward you passively without any redemption management. The single most important rule at this stage: pay the full statement balance every month, not just the minimum. One month of carrying a ₹15,000 balance at 40% APR erases six months of cashback earnings. For a detailed breakdown of first-card options by eligibility, see best credit cards for students and first-timers in India.

Is a lifetime free credit card always better than a paid card?

Not always, and often the opposite is true. Lifetime free cards have no recurring fee revenue to fund high reward rates, so most LTF cards earn 0.5–1% on general spends. A ₹499/year paid card earning 3–5% on your primary spend category typically outearns an LTF card earning 1% by ₹3,000–₹5,000 annually at moderate spend levels. The Amazon Pay ICICI is the notable exception: 5% LTF cashback on Amazon is genuinely excellent for a zero-fee card. The right test: take your top monthly spend category, multiply by the paid card's earn rate minus the LTF card's earn rate, and multiply by 12. If that number exceeds the annual fee, the paid card wins. At ₹20,000/month total spend, Axis ACE (₹499/year, 1.5% flat) returns roughly ₹6,200 net after fee, significantly more than most LTF cards on the same spend.

About the Author

Anmol Ratan Sachdeva

Anmol has been tracking the Indian credit card market since 2019, reviewing benefits, changes across 40)+ cards and documenting issuer devaluations in real time. He personally has a card portfolio across HDFC, Axis, SBI Card, ICICI, and writes from direct usage experience. His analysis focuses on real-world return calculations rather than headline reward rates. He writes content for educational purposes.