HDFC Infinia Credit Card 2026: Real Experiences from Real Voices

Last updated on

HDFC Infinia is invite-only. Reddit cracked how to get it and if the chase worth it? Here's the real experience...

Too busy to read endless reviews & research?

Find the best cards that suit your lifestyle in 30 seconds

Try Monzy NowNo signup or email required

My neighbor Rajesh got his HDFC Infinia back in 2022. He was over the moon about it then, showing off the metal card and talking about unlimited lounge access like he'd won the lottery.

Fast forward to today, he is genuinely confused about whether to keep the card or not. A few weeks back, he woke up to an email about relationship value for Infinia by HDFC.

He was not alone. Across r/CreditCardsIndia last year, threads about sudden Infinia downgrades were appearing faster than HDFC's customer care could handle the calls.

Holders who had never missed a payment found themselves holding an HDFC Regalia Gold instead of the metal card they had spent years building toward.

That experience shaped how I approached this review when I first wrote this. But since then, things have moved further: HDFC introduced a full retention overhaul in early 2026, a voucher earn-rate cut, and new redemption limits.

The card my neighbor held is materially different from the one being offered today, and not everyone has caught up on the changes.

So, here I am with Infinia pros and cons for 2026.

TL;DR

The HDFC Infinia Metal delivers genuine best-in-class returns for an HNI looking for a credit card. They need to spend above ₹1.5 lakh a month and redeem primarily through SmartBuy travel bookings for best benefits.

Below ₹1 lakh a month, the ₹14,750 annual fee (after GST) is hard to recover. A new April 2026 rule requires either ₹18 lakh in annual spend or ₹50 lakh in HDFC deposits to keep the card, which changes the calculation entirely now.

Quick Spec Sheet for Infinia

Feature | Details |

Annual Fee | ₹12,500 + GST = ₹14,750 |

Joining Fee | ₹12,500 + GST |

Fee Waiver | ₹10L annual spend |

Card Retention (2026) | ₹18L annual spend OR ₹50L RLV |

Earn Rate | 5 pts per ₹150 (3.33 pts/₹100) |

SmartBuy Accelerator | Up to 10X on travel/shopping |

SmartBuy Bonus RP Cap | 15,000 bonus RP per calendar month |

Redemption Cap | 5 redemptions/month; ₹50,000/month against statement balance; ₹2,00,000 per statement cycle (overall); ₹1,50,000/month for flights, hotels and airmiles combined |

Point Value (best case) | ₹1/pt via SmartBuy travel or Apple/Tanishq |

Point Value (vouchers) | ~₹0.20–₹0.50/pt for product catalogue vouchers; ₹0.30/pt for statement credit (cashback) |

SmartBuy Voucher Accelerator | 5X on Gyfter |

70% Travel Booking Cap | Points cover up to 70% of SmartBuy travel; 30% by card |

Points Expiry | 3 years from accrual date |

Forex Markup | 2% + GST (~2.36%) |

Domestic Lounge | Unlimited — primary and add-on (DreamFolks) |

International Lounge | Unlimited — primary and add-on (Priority Pass) |

Network | Visa |

Infinia out of reach right now? get a personalised credit card recommendation →

Who The Infinia Metal Card is Actually For?

The Infinia Metal is not designed for someone spending ₹40,000 to ₹60,000 a month. The annual fee alone works out to roughly ₹1,230 per month, and getting meaningful value back requires a specific combination of spending volume and redemption discipline.

This card makes sense if you:

- Spend ₹1.5 lakh or more per month across different expenses combined;

- Travel two or three times a year and care about lounge access on both domestic and international routes;

- Are comfortable redeeming points through HDFC SmartBuy rather than converting to vouchers;

- Have or are willing to build a strong HDFC banking relationship through savings account, FD, or investment products, given the new 2026 retention criteria

If your salary account is elsewhere and you hold the Infinia purely as a standalone credit card, your position at renewal is less certain than it was two years ago. I'll get into exactly why in the eligibility section.

For context on where the Infinia sits in the full HDFC Bank credit card range, it is the bank's most exclusive product, above the Regalia Gold, the Diners Black, and every co-branded card in the portfolio.

The Reward Maths: What You Actually Earn in 2026

The Base Rate

The earn rate is 5 Reward Points per ₹150 spent. That works out to 3.33 points per ₹100. Fuel transactions are excluded from earning.

One Reward Point is not worth ₹1 universally. The route you use to redeem makes a large difference.

- Route 1: SmartBuy travel bookings (full value). Redeeming against flights or hotel bookings via HDFC SmartBuy gives you 1 Reward Point = ₹1. This is the only way to get close to the headline 3.33% return that card comparison sites cite. One important constraint: you can only use points for up to 70% of a travel booking, the remaining 30% must be charged to the card.

- Route 1B: Apple products and Tanishq vouchers. Also 1 Reward Point = ₹1, with the same 70% booking cap. This is a route most holders are not aware of, and it is genuinely useful if you have a large purchase coming up in either category.

- Route 2: General vouchers via SmartBuy Gyftr. General vouchers via SmartBuy Gyftr. Infinia continues to earn 5X points on brand voucher purchases (1X base + 4X bonus), translating to roughly 16.5% effective return on vouchers like Amazon Pay before processing fees. HDFC announced a cut to 3X effective 16 January 2026, but reversed the change on 15 January after cardholder backlash. The 5X rate remains in force as of mid-2026.

- Route 3: Statement balance or other products. Approximately ₹0.30–₹0.50 per point. Worth using only for expiring points you cannot redeem elsewhere.

SmartBuy Accelerator Program

On SmartBuy, Infinia earns up to 10X on travel and shopping. The monthly bonus RP cap from the SmartBuy accelerator is 15,000 points per calendar month.

Once you hit that cap, subsequent SmartBuy purchases earn at the base 1X rate. If you are booking a ₹3–4 lakh international itinerary, plan across two billing months to capture the accelerator across both.

The Spend Maths Table for Infinia in 2026

Monthly Spend | Annual Spend | Points Earned | Value at SmartBuy (₹1/pt) | Value at Voucher (₹0.50/pt) | Annual Fee (incl. GST) | Net Value — SmartBuy | Net Value — Voucher |

₹50,000 | ₹6,00,000 | 19,980 | ₹19,980 | ₹9,990 | ₹14,750 | +₹5,230 | -₹4,760 |

₹1,00,000 | ₹12,00,000 | 39,960 | ₹39,960 | ₹19,980 | ₹14,750 | +₹25,210 | +₹5,230 |

₹2,00,000 | ₹24,00,000 | 79,920 | ₹79,920 | ₹39,960 | ₹14,750 | +₹65,170 | +₹25,210 |

Points calculated at base 3.33/₹100 only. SmartBuy accelerator earnings excluded. ₹14,750 = ₹12,500 fee + 18% GST.

The ₹50,000/month picture is uncomfortable. You are barely in the black at SmartBuy, and actively losing money if your redemption is through general vouchers. Anyone recommending the Infinia for moderate spenders is not running this maths.

At ₹1 lakh per month the case stacks up, particularly on the SmartBuy path. At ₹2 lakh per month, the returns justify the premium positioning clearly.

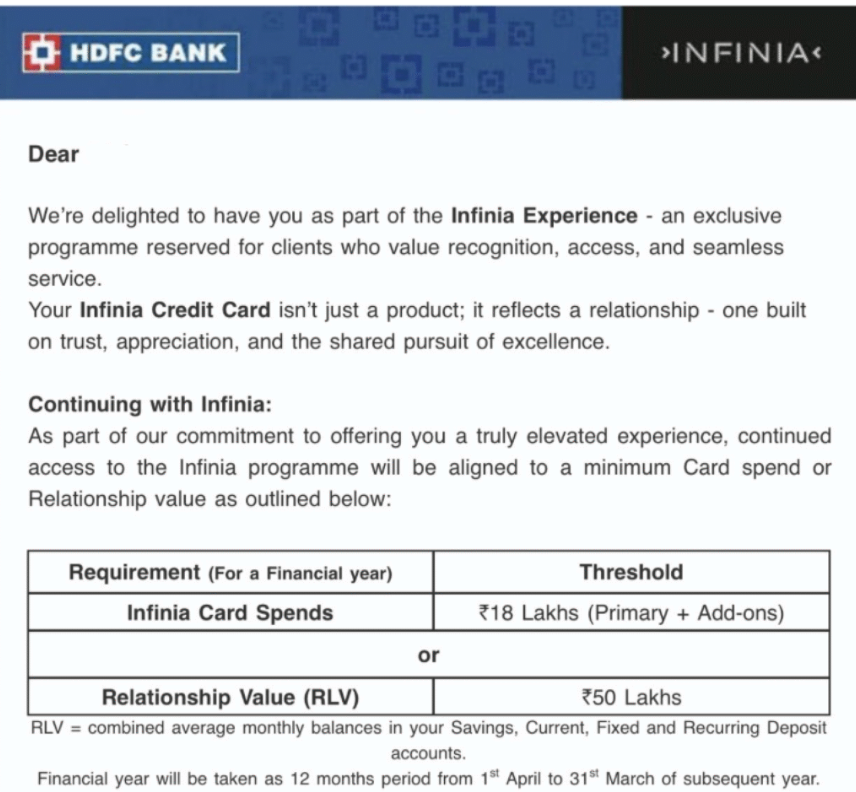

Annual Fee, Fee Waiver, and the 2026 Retention Rule for Infinia

There are now two distinct thresholds you need to know about, and most reviews are conflating them. They are not the same thing.

- Fee waiver (still ₹10 lakh): Spend ₹10 lakh or more in the preceding 12 months and HDFC waives the ₹12,500 annual fee. This threshold has not changed. At ₹83,333 per month, it is achievable if the Infinia is your primary card for business and personal spend combined.

- Card retention (new from April 2026): To keep the Infinia programme at all, not just waive the fee, but stay in the programme, you now need to meet one of two conditions each financial year: spend ₹18 lakh on the card (primary plus add-on combined), or maintain a Relationship Value of ₹50 lakh with HDFC Bank across savings accounts, current accounts, FDs, and recurring deposits. Cardholders who do not meet either criterion risk a forced downgrade in 2027.

These are separate bars. You could spend ₹10 lakh (qualifying for the fee waiver) and still fail the retention threshold. For anyone spending in the ₹10–17 lakh per year range, that is a meaningful gap to close.

I have written about how annual fee waivers actually work in India separately, including which spend categories typically count and which do not. The short version: fuel, EMI conversions, and rent payments usually do not count toward the waiver calculation.

Lounge Access on HDFC Infinia Credit Card

The Infinia Metal comes with unlimited domestic and international airport lounge access.

HDFC issues a Priority Pass card to both the primary and add-on cardholder as part of the welcome kit. The add-on holder presents their own Priority Pass card at international lounges, not as a guest of the primary cardholder, which means there is no cap, no per-visit charge, and no spend requirement attached.

This is a genuine competitive edge. If you have issued an add-on card for a spouse or parent, both of you can access lounges independently and without restriction.

Axis Magnus, which frequently gets compared to the Infinia, has spend-gated its lounge benefit since mid-2024. The Infinia has no such spend gates.

If you want a full breakdown of which Indian airport lounges are accessible and how to navigate the DreamFolks system, the credit card lounge access guide covers this in detail.

Forex and International Spends on HDFC Infinia

The forex markup is 2% + GST, which works out to approximately 2.36% all-in on international transactions. For a card at this price point, that is not zero, it is worth knowing before you land in Singapore and start swiping.

The partial offset comes from the earn rate. You still earn 3.33 points per ₹100 on international spend, which returns roughly 3.33% at SmartBuy.

Net-net, after the forex cost, you are slightly ahead on international transactions if you are redeeming at full SmartBuy value. But if you are on the general voucher route, the forex markup tips you into marginal or negative territory on overseas spend.

For pure international travel spend, a zero-forex card as a companion card alongside the Infinia is a reasonable approach. The Infinia handles everything else; the zero-forex card handles the currency conversion.

The 2026 Eligibility and Retention Shake-Up for Infinia

Recently, HDFC tightened the Relationship Value criteria for existing holders, leading to a wave of unannounced downgrades that upset a lot of long-time cardholders. Threads on r/CreditCardsIndia from October through December 2024 were full of people who had received a Regalia Gold in the post and had no idea why.

From April 1, 2026, HDFC has introduced formal annual continuity criteria for the Infinia programme. To keep the card at the end of the 2026–27 financial year, cardholders must meet one of two conditions:

- Spend ₹18 lakh on the Infinia card during April 1, 2026 to March 31, 2027 (primary and add-on card combined), or

- Maintain an average monthly Relationship Value of ₹50 lakh with HDFC Bank across deposits

The ₹18 lakh spend target works out to ₹1.5 lakh per month. That is achievable for high-volume spenders, but it requires the Infinia to be your actual primary card, you cannot route most of your spend elsewhere and keep the card for occasional SmartBuy bookings.

HDFC has been explicit that it is clearing out holders who treat the Infinia as a lounge card while routing real spend to other products.

The ₹50 lakh RLV path is the one for business owners and HNIs who already hold significant deposits with HDFC. If you hit this, the card spend threshold becomes irrelevant.

The broader pattern of Indian banks recalibrating premium card economics in 2025–26, not just HDFC, is worth understanding if you hold multiple premium cards. I covered this in the 2026 Indian credit card devaluation roundup.

Hidden Conditions about Infinia Worth Knowing in 2026

The 15,000 bonus RP monthly SmartBuy cap. The 10X accelerator on SmartBuy is capped at 15,000 bonus reward points per calendar month. If you are booking international flights costing ₹2 lakh or more in one transaction, you will not earn 10X on the full amount. Plan large bookings across months where possible.

Maximum 5 redemptions per month. From 1 February 2026, HDFC limits Infinia cardholders to 5 redemption requests per calendar month. Statement balance redemption is capped at 50,000 reward points per month (worth roughly ₹15,000 in statement credit at 1 RP = ₹0.30). The overall cap is 2,00,000 reward points per statement cycle, with 1,50,000 RP/month sub-cap on flights, hotels and airmiles combined.

SmartBuy voucher devaluation (January 2026). HDFC announced a cut from 5X to 3X on Gyftr voucher purchases effective 16 January 2026 but rolled it back on 15 January, before the change went live. The 5X rate (roughly 16.5% effective on vouchers like Amazon Pay) remains in force, though HDFC has signalled intent to revisit this and cardholders should monitor SmartBuy T&Cs.

The 70% booking cap on travel. You can only pay with reward points for up to 70% of a SmartBuy travel booking. The remaining 30% is charged to the card. This is not a problem in itself — the 30% card spend continues to earn points, but it is a constraint to factor into redemption planning for large bookings.

Points expiry: 3 years. Infinia reward points are valid for 3 years from the date of accrual. This is longer than standard HDFC cards (typically 2 years) but still finite. Points also lapse entirely if the card is not used for 365 consecutive days.

Rental payments do not earn points. Transactions through platforms like NoBroker or housing rent payment services do not earn Reward Points and do not count toward the annual fee waiver spend. If rent is a large share of your monthly spending, the effective earn rate is lower than the headline number suggests.

Cash advance: avoid entirely 2.5% of the amount or ₹500, whichever is higher. There is no scenario where using an Infinia Metal for a cash advance makes financial sense.

Pros and Cons for HDFC Infinia Credit Card

Pros | Cons | |

|---|---|---|

General | The 3.33% base earn rate is genuinely good. Most cards at ₹12,500+ annual fee deliver lower effective returns across everyday spend. | The ₹18 lakh annual spend requirement for retention makes the card high-maintenance if the Infinia is not your primary card. Holding it casually while routing real spend elsewhere is no longer viable. |

Travel | Unlimited lounge access for both primary and add-on cardholders, without any spend gate, remains a significant advantage, especially as competitors tighten their lounge benefit terms. | For cardholders outside major metros with fewer direct international flights, the Priority Pass benefit is less useful in practice than on paper. |

Points Redemption | The SmartBuy 10X accelerator, even with the monthly cap, delivers returns that no other bank's portal currently matches. If you book ₹1.5 lakh of flights and hotels per month through SmartBuy, you are pulling ₹15,000+ in reward value just from the accelerated earning. | The SmartBuy platform has real inventory limitations. Discount fares on budget airlines often do not appear on SmartBuy, and hotel pricing sometimes runs higher than Booking.com or MakeMyTrip. The portal has improved but it is not seamless, and that affects how much of the accelerator benefit you can practically capture. |

Memberships & Lifestyle Perks | The Marriott Club membership, ITC hotel benefits, and 24/7 concierge are legitimate lifestyle perks, not just marketing padding, if you use them. | HDFC has telegraphed its intent to cut voucher rates (the 5X to 3X change was announced and reversed within 24 hours in January 2026). The 5X rate currently stands, but cardholders should plan voucher-heavy strategies cautiously given the bank's clear direction of travel. |

What Real Users on Reddit Actually Think?

The mood on online forums and Reddit about the Infinia has shifted over the past 18 months. The card used to be the automatic "best answer" to any premium card question on the sub. That consensus has softened.

The most common thread types now:

- The downgrade thread is a near-weekly occurrence. Holders who had the card for years, with clean repayment history, received quiet downgrades to Regalia Gold after the 2024 RLV tightening. The shock was less about losing the card and more about HDFC's communication style: no warning, no explanation, a new card in the post.

- The "should I switch" thread has become genuinely competitive. A year ago, most commenters would push back in favour of Infinia. Now the sub is more split, particularly among users who travel internationally and want airline miles rather than portal credits.

- The SmartBuy frustration thread is legitimate. Inventory problems like flights not showing, hotel prices running higher than competitor sites, are a recurring complaint from Infinia holders trying to extract the SmartBuy benefit. The 10X is attractive; the portal does not always cooperate.

- The ₹18 lakh rule thread is new in 2026, and sentiment is mixed. High-volume spenders see it as a reasonable bar. Holders spending ₹8–12 lakh per year are frustrated, particularly if they have held the card for years and used it loyally within their actual spend capacity.

Real Approval Stories about Infinia from Past 1 Year

- The Corporate Route: Amit from Mumbai got his through his company's tie-up with HDFC. His IT firm had a corporate banking relationship, and employees with ₹30+ lakh salaries were offered Infinia as part of the package.

- The Relationship Route: Sunita, a small business owner from Jaipur with ₹40 lakh ITR, struggled for months despite her income. She finally got it after moving her business account to HDFC and maintaining a ₹25 lakh average balance for six months.

- The Upgrade Path: Rohit upgraded from Diners Club Black after two years. His monthly spending of ₹1.2 lakhs caught HDFC's attention, and they offered the upgrade without him asking. The Diners Black is often the card HDFC watches before offering you the Infinia. If you are currently on it and wondering whether to stay or upgrade, our HDFC Diners Black review walks you through exactly when the switch makes sense.

The backdoor methods people talk about on Reddit do work, but they come with real costs.

The ₹50 lakh FD route is legitimate: you can get Infinia against a fixed deposit of this amount. But ask yourself: is tying up ₹50 lakhs to get a credit card really worth it when that money could earn you ₹3-4 lakhs annually in better investments?

What doesn't work are the myths about salary certificates or income manipulation. HDFC's verification process has gotten stricter, not looser. They cross-check ITR filings, bank statements, and employment records more thoroughly than ever.

So, the exclusivity feels increasingly artificial in 2026.

With so many premium cards offering similar benefits at lower thresholds, HDFC's invite-only approach seems more about maintaining brand prestige than actual risk management.

HDFC Infinia Metal vs Axis Magnus

This comparison comes up constantly, because both cards are targeting the same person. Here is how they stack up at ₹1 lakh per month in general spend, with travel booked via each bank's portal.

Feature | HDFC Infinia Metal | Axis Magnus |

Annual Fee (incl. GST) | ₹14,750 | ₹14,750 |

Fee Waiver Threshold | ₹10L/year spend | ₹25L/year spend |

Retention/RLV Threshold | ₹18L spend or ₹50L RLV | ₹30L NRV with Axis Burgundy |

Base Earn Rate | 3.33 pts/₹100 | 3 pts/₹100 equivalent |

Travel Portal Accelerator | Up to 10X on SmartBuy (15K RP/month cap) | 12 EDGE Miles/₹200 on Travel Edge |

Point Value (best case) | ₹1/pt via SmartBuy travel | ₹0.20/pt direct; transfers to airline miles at 5:4 |

Forex Markup | ~2.36% | ~2.36% |

Domestic Lounge | Unlimited (primary + add-on) | Unlimited but spend-gated from 2024 |

International Lounge | Priority Pass — unlimited (primary + add-on) | Priority Pass — unlimited |

Best For | SmartBuy rupee-value redemptions | Airline miles and hotel loyalty transfers |

The decision comes down to how you want to use rewards. Infinia gives you straightforward rupee value: book travel on SmartBuy, get 10X, redeem at ₹1 per point. No complexity, no transfer ratios, no availability windows. If you do not want to become a miles strategist, Infinia is the simpler path.

Magnus is for someone who gets real value from flying business class on redeemed miles or staying in Marriott properties using transferred points. The EDGE Miles ecosystem has more transfer partners than Infinia's programme, and if you know how to extract value from that, the Magnus can outperform the Infinia at equivalent spend.

I have written a full Axis Magnus review separately. If you are choosing between the two, read that alongside this piece before deciding.

The Infinia also compares differently to the ICICI Emeralde Private Metal — a card that is increasingly coming up in premium card discussions for its straightforward cashback structure and no-spend-gate lounge access.

The Case Against the Infinia Metal

I want to spend a moment on this because most reviews rush to the verdict.

- If your spending is primarily offline and domestic, groceries, dining, kirana bills, the Infinia's strongest returns require SmartBuy redemption for travel. A high-spending household that does not travel regularly will leave a significant portion of the card's value untapped.

- If your primary banking relationship is with another bank, the ₹50 lakh RLV path to retention is not available to you, and the ₹18 lakh spend path requires the Infinia to be your main card. That is a commitment worth making deliberately rather than by default.

- If zero forex markup matters to you, the Infinia's 2.36% cost on international transactions is real. For frequent international travellers whose single biggest spend category is overseas, a zero-forex companion card or a more travel-specialised product may serve the wallet better.

- If airline miles strategy is how you prefer to travel, Magnus's transfer partnerships give you more flexibility than what SmartBuy currently offers. The Infinia's strength is straightforward portal value, not miles arbitrage.

- If after running your own numbers the Infinia still does not fit, whether that is because of the spend bar, the SmartBuy dependency, or the forex cost, the best travel credit cards in India shortlist is a more useful starting point than forcing a premium card that does not match your wallet.

The Verdict

The HDFC Infinia Metal is not overrated. At ₹1.5 lakh or more in monthly spend, with a strong HDFC relationship and the discipline to book travel through SmartBuy, this card delivers returns that most premium cards in India cannot match.

But the 2026 changes have raised the bar for keeping it. The ₹18 lakh spend requirement is not punishing for people who already use the Infinia as their primary card, they were hitting close to that anyway. For everyone else, it is a forcing function: either commit to the card or let it go.

My honest read: if you comfortably spend above ₹1.5 lakh per month, have a meaningful HDFC banking relationship, and will actually use SmartBuy for travel, get the Infinia if you receive the invite. The maths work, the lounge access is genuinely superior to most competitors right now, and the SmartBuy accelerator is still the most rewarding portal in the Indian market.

If you are stretching to qualify, or your HDFC relationship is thin, or you are spending ₹80,000–₹1 lakh per month and hoping it gets better, look at the Axis Magnus, the Regalia Gold, or the ICICI Emeralde first. The Infinia at below-breakeven spend is an expensive status symbol. At the right spend level, it is one of the best cards available.

Frequently Asked Questions

What is the annual fee for HDFC Infinia Metal, and can it be waived?

The annual fee is ₹12,500 + 18% GST = ₹14,750. It is waived if you spend ₹10 lakh or more in the preceding 12 months. Fuel purchases, EMI conversions, and rent payments typically do not count toward this threshold.

What are the new 2026 retention rules for HDFC Infinia?

From April 2026, Infinia cardholders must meet one of two conditions in the financial year to keep the card: spend ₹18 lakh on the Infinia (primary and add-on combined), or maintain a Relationship Value of ₹50 lakh with HDFC Bank across deposits. This is separate from the fee waiver threshold of ₹10 lakh.

Do add-on cardholders on HDFC Infinia get unlimited lounge access?

Yes. Both primary and add-on cardholders receive unlimited domestic and international lounge access. HDFC issues a Priority Pass card to add-on holders as part of the welcome kit, so they access lounges independently — not as a guest of the primary cardholder.

What is the forex markup on HDFC Infinia?

2% + GST, approximately 2.36% all-in on international transactions. You continue to earn base reward points on international spend, which partially offsets this cost if you redeem at SmartBuy value.

How many reward points do I earn on HDFC Infinia, and what are they worth?

5 Reward Points per ₹150 spent (3.33 points per ₹100). At SmartBuy travel redemption, 1 point = ₹1. At general vouchers, 1 point = approximately ₹0.50. At statement balance, 1 point = approximately ₹0.30. Note you can only use points for up to 70% of a SmartBuy travel booking.

Is HDFC Infinia better than Axis Magnus?

For straightforward rupee-value returns via HDFC SmartBuy, Infinia typically edges out Magnus. For airline miles accumulation and flexible loyalty transfers, Magnus has more partner depth. The right choice depends on whether you prefer portal-based travel value or a miles strategy.

What changed on HDFC Infinia in 2025–26?

Several things: the SmartBuy brand voucher accelerator dropped from 5X to 3X (January 2026); redemptions are now capped at 5 per month with a ₹50,000 monthly statement balance limit; the card retention rule moved to ₹18 lakh spend or ₹50 lakh RLV (April 2026); and the 2024 RLV tightening led to widespread unannounced downgrades that continued into 2025.

Can HDFC Infinia be downgraded without notice?

It has happened. Since the 2024 RLV tightening, holders with thin HDFC banking relationships received forced downgrades to Regalia Gold without prior communication. The April 2026 retention rule means this risk is now formalised — non-compliant holders will be notified in 2027 and face downgrade or removal from the programme.

Related Reading

About the Author

Sakshi Dubey

Sakshi loves to shop and uses credit cards to understand how she can minimize her spending and maximize rewards. She writes posts about credit card rewards, best cards for everyday spends, and guides on optimizing credit card usage.