The Great Indian Credit Card Devaluation

Last updated on

The one-card era is dying. Here's the math and rules driving India's 2026 credit card reset and what you should do after SBI Cashback Card devaluation.

Table of Content

When the SBI Cashback Credit Card slashed its benefits, it wasn't acting alone. It joined a growing wave of devaluations sweeping across major issuers like Axis, ICICI, and HDFC Bank.

Make no mistake: this isn't a coordinated attempt to pad quarterly margins. We are witnessing a systemic reset. It is an inevitable correction driven by three inescapable realities:

- Macroeconomic Shifts: Changing interest rates and capital costs.

- RBI Regulatory Clampdowns: Stricter guidelines on co-branded cards and capital requirements.

- Unit Economics: The mathematical limits of funding massive reward structures in India's maturing digital payments ecosystem.

Between RBI regulatory clampdowns, shifting macroeconomic winds, and the harsh reality of payment unit economics, the old rewards models are no longer sustainable.

Here is a breakdown of exactly what is forcing the hands of Indian banks today:

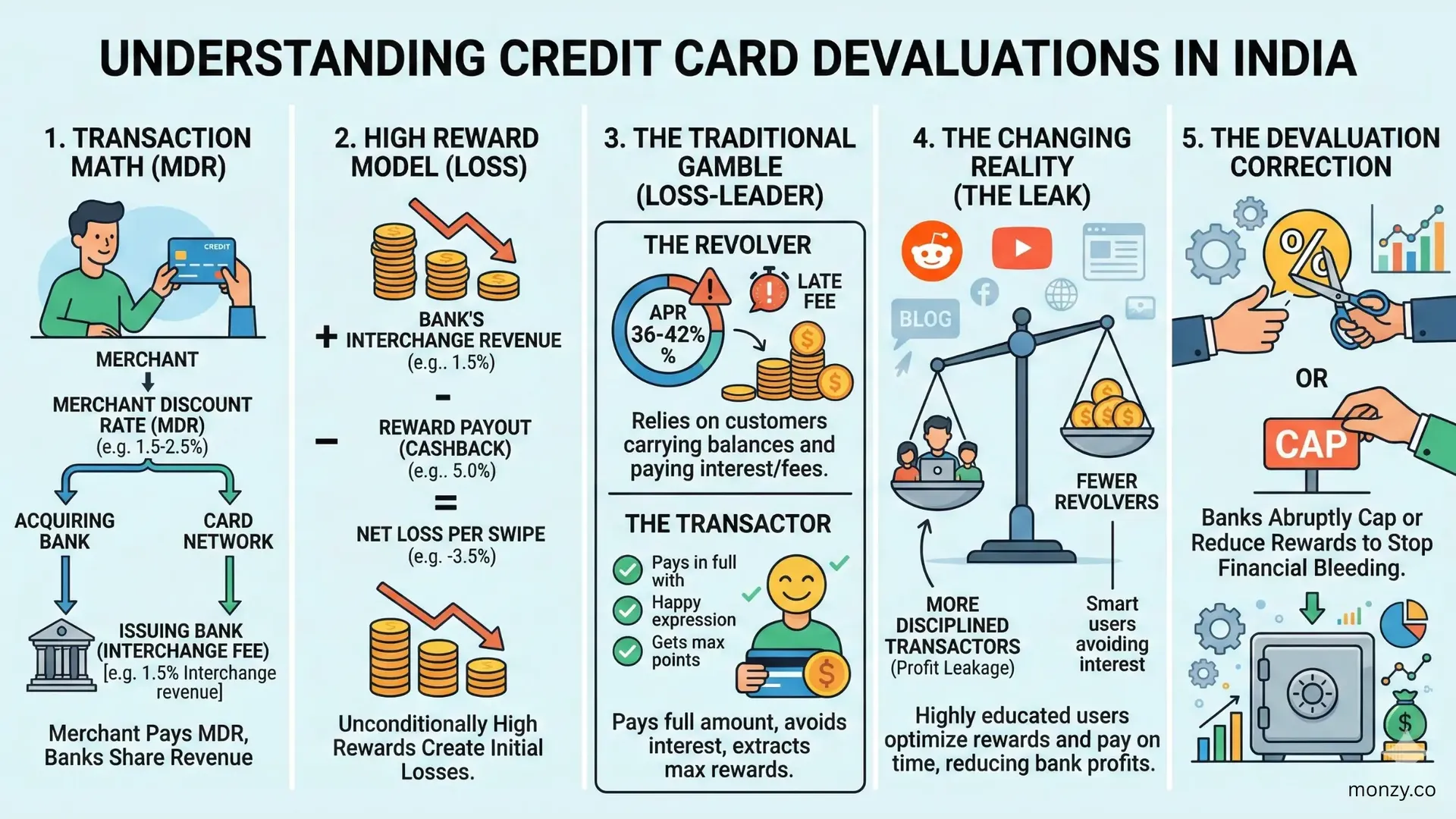

The Brutal Reality of Merchant Discount Rates (MDR)

To understand the inevitability of these mass devaluations, you must conduct a clinical examination of the underlying unit economics of a standard credit card transaction.

When you make a purchase, the merchant pays a Merchant Discount Rate (MDR), typically fluctuating between 1.5% and 2.5% in India. This revenue is split between the acquiring bank, the card network, and the issuing bank (which receives the "Interchange Fee").

Math That Doesn't Add Up in 2026

Look at the numbers on a card offering a flat 5% cashback:

- Bank's Actual Revenue (Interchange): ~1.2% to 1.8%

- Bank's Payout to Customer (Cashback): 5.0%

- Net Loss per Swipe: ~3.2% to 3.8%

The "Loss-Leader" Bet

Why would banks willingly absorb this loss? They rely on statistical models predicting that a portion of users will fail to clear their total amount due.

These "revolvers" carry balances subjected to exorbitant annualized percentage rates (APR) of 36% to 42%, alongside highly profitable late fees. The massive rewards are bait to acquire these profitable accounts.

Rise of the "Transactor" Army

However, the Indian retail landscape has undergone a radical transformation. Powered by active Reddit communities, YouTube finfluencers, and dedicated blogs, digital financial literacy has skyrocketed.

This created a massive demographic of highly disciplined "transactors": educated optimizers who ruthlessly extract maximum rewards, but religiously pay their bills in full, on time, every single month. They never trigger a single rupee of interest.

Result: The House Begins to Lose

When a credit card portfolio becomes overly saturated with perfectly disciplined transactors, the product transitions from an acquisition cost into a structural, bleeding liability.

Abruptly capping online cashback (like limiting it to ₹2,000) is simply the banking sector attempting to push a patch. They are stopping the financial bleeding caused by a demographic of high-spending optimizers who finally outsmarted the statistical models.

RBI’s Regulatory Squeeze

While failing unit economics played a massive role, the ultimate catalyst for the 2026 wave of devaluations was the Reserve Bank of India (RBI) stepping in to cool down an overheating market.

Over the past decade, the Indian credit card market operated in a state of hyper-growth.

Active credit cards in circulation surged an astonishing fivefold, expanding from a mere 55 million in FY20 to a massive 111 million by FY25 with a 20% Compound Annual Growth Rate (CAGR).

This brought credit to millions, but it also triggered severe regulatory alarm bells regarding unbacked consumer debt.

Warning Signs

In late 2025, the RBI's Financial Stability Report flagged rapidly rising, systemic risks in unsecured retail lending:

- Rising Debt: The average outstanding balance per card surged from ₹28,919 to ₹32,233, showing consumers heavily relying on debt to fund lifestyle inflation.

- Increasing Defaults: Gross Non-Performing Assets (GNPA) in unsecured retail climbed to 107 basis points by late 2025.

- Early Warning Indicators: Delinquency rates in the critical 91–180 days past due (DPD) category, a strong precursor to total default, jumped from 6.5% to 7.6%.

- Private Bank Exposure: Private sector banks accounted for a disproportionate 76% of all slippages in unsecured retail loans.

The Crackdown

In direct response to these deteriorating metrics, the RBI enacted strict macro-prudential reforms:

- Higher Risk Weights: The RBI forced banking institutions to hold significantly more of their own capital in reserve against their outstanding credit card balances.

- Expected Credit Loss (ECL) Mandate: By April 2027, all Indian banks must adopt a forward-looking ECL framework. Instead of waiting for a loan to default, banks must account for potential future losses the moment the card is issued.

Overnight Change in the Ecosystem

With the regulations in play, the financial arithmetic for Indian banks changed almost instantly.

- Drastically higher capital provisioning requirements will lock up liquidity, and;

- Tighter compliance costs will squeeze bank’s margins.

This means banks can no longer afford to subsidize massive, frictionless 5% cashback programs while simultaneously being forced by the central bank to sit on vast, unproductive cash reserves for potential defaults.

Slashing reward systems became the most immediate way to offset these heavy, newly mandated regulatory costs.

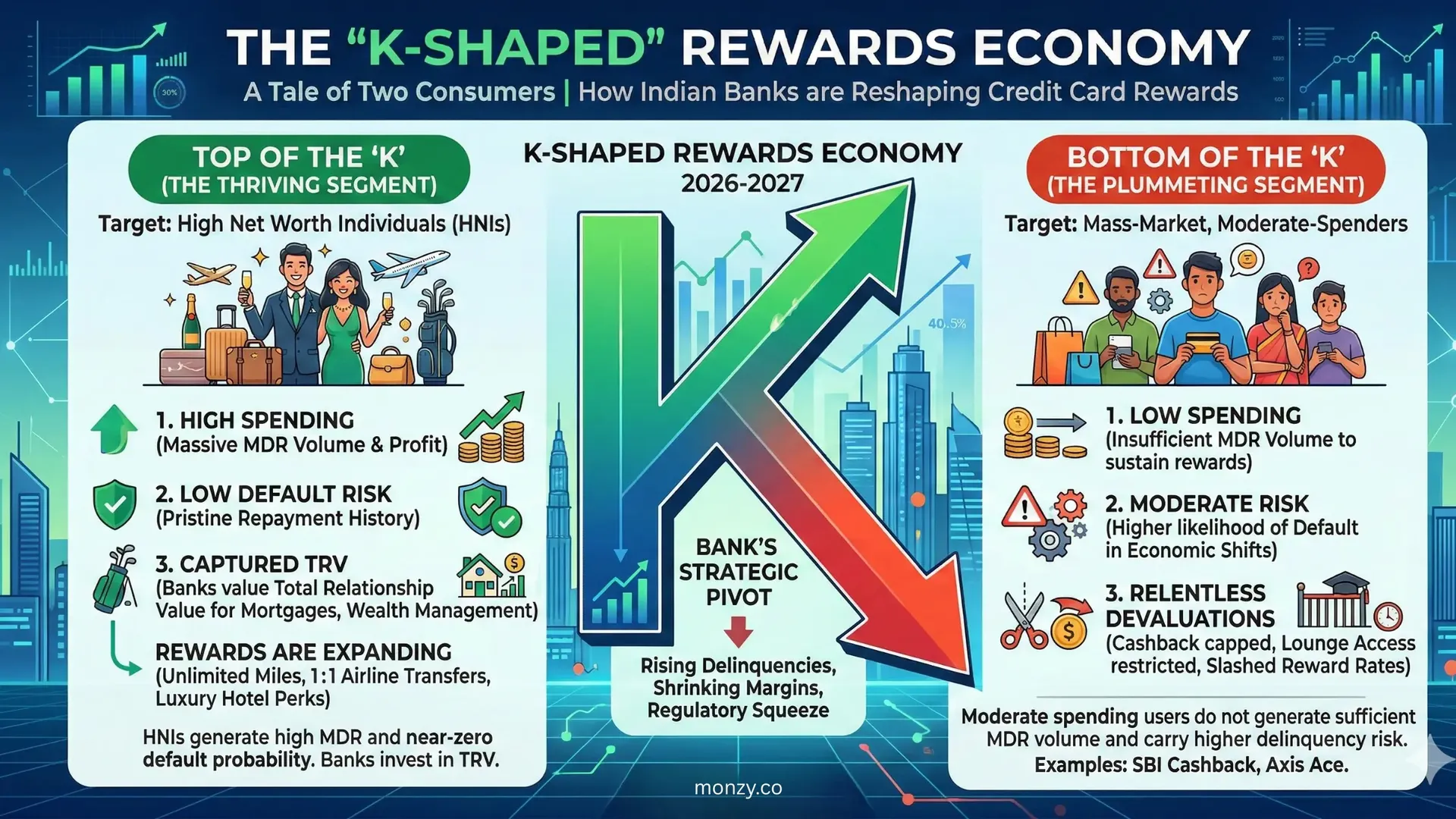

The "K-Shaped" Rewards Economy: Tale of Two Consumers

Faced with rising delinquencies and shrinking margins, banks may execute a hard strategic pivot.

Many issuers might be slowly moving away from generic, mass-market acquisition and focusing almost entirely on securing high-income, deeply entrenched urban users with pristine repayment histories.

This shift has created a distinct "K-shaped" rewards economy.

Just like a K-shaped economic recovery where one segment thrives while another plummets, the credit card market is splitting into two entirely different realities based on the user's wealth and spending habits.

Here is how the new benefit equation breaks down:

The Benefit Equation | Top of the 'K' | Bottom of the 'K' |

Target Audience | High Net Worth Individuals (HNIs) | Moderate-spending, mass-market consumers |

Card Types | Ultra-premium, invite-only cards | Entry-level & mid-tier (SBI Cashback, Axis Ace) |

The Bank's View | High MDR volume, near-zero default risk. High Total Relationship Value (TRV) for cross-selling mortgages and wealth management. | Low MDR volume. Higher statistical probability of default if macroeconomic conditions worsen. |

The Reward Reality | Expanding Perks: Lucrative 1:1 airline transfers, luxury hotel value (up to 33% return), and exclusive golf access remain fully funded. | Relentless Devaluations: Cashback capped, lounge access restricted, and baseline reward rates slashed to stop financial bleeding. |

This sentiment was also highlighted in a recent discussion on Reddit about the devaluation situation, too.

The Demise of "Arbitrage Spends"

Another core driver of the 2026 devaluations is the aggressive, industry-wide crackdown on points arbitrage, commonly known as "manufactured spending."

Historically, highly educated users exploited multi-layered, gamified systems to earn outsized rewards on mandatory expenses. The financial industry has moved uniformly to crush these workarounds.

The Loophole vs. The Crackdown:

- The Loophole: Users would buy Amazon Pay gift vouchers at a 5% discount using premium cards, then use that wallet balance to pay utility bills, school tuition, or insurance, categories that normally yield zero rewards due to exceptionally low base MDRs.

- The Fee Penalty: To stop this, banks are imposing new costs. For example, ICICI Bank recently imposed a punitive 1% fee on third-party wallet loads exceeding ₹5,000 and removed accelerated rewards on iShop vouchers.

- Expanding Exclusions: Banks are drastically expanding their lists of excluded Merchant Category Codes (MCCs). SBI, for instance, has entirely cut off rewards for government taxes, tolls, and gaming platforms.

- AI Intervention: Banks are now heavily leveraging real-time behavioral scoring algorithms and sophisticated AI to accurately distinguish genuine retail consumption from gamified arbitrage, instantly stripping rewards from the latter.

Adapting to the New Reality: The End of the "One-Card" Era

The recent devaluation of the SBI Cashback Credit Card may finally serve as a tombstone for the golden era of hyper-rewarding, frictionless, single-card setups in the Indian retail market.

The simplistic days of applying for one universally powerful piece of plastic, automating all household and lifestyle spends through it, and passively yielding a massive 5% return across the board are over.

Indian credit card ecosystem is maturing: banking risk models are now highly sophisticated, and the RBI aggressively prioritizes systemic banking stability over unchecked consumer growth.

Building a Purpose-Built Digital Wallet

For the digitally savvy consumer, the path forward is complex but clear. It requires a fundamental transition away from simplistic brand loyalty toward ruthless, strategic portfolio management.

Optimizing financial returns in 2026 and beyond necessitates the construction of a fragmented, purpose-built digital wallet. You must now compartmentalize your spending to extract maximum value:

- High-Volume E-commerce: Route through co-branded cards like the Amazon Pay ICICI card.

- Daily Dining & Food Delivery: Capture accelerated value via the HDFC Swiggy card.

- Offline Household Groceries: Anchor physical retail spending with the HSBC Live+.

- Generalized Digital Spending: Utilize the BOBCARD Cashback as a controlled instrument for unmapped online purchases.

As the Indian banking sector braces for the full implementation of the stringent Expected Credit Loss (ECL) framework by April 2027, consumers should anticipate even further tightening of benefits.

So, now the credit card game in India is no longer about blindly finding a single "golden ticket." It is a meticulous, ongoing, and highly mathematical exercise in dynamic arbitrage, rigorous expense categorization, and disciplined financial architecture.

Also Read: Best Credit Card Alternatives for SBI Cashback Credit Card after Devaluation

About the Author

Anmol

Anmol writes detailed blogs and content about credit cards available in India and how to take full advantage of credit cards while avoiding marketing noise.