Best SBI Cashback Alternatives After the April 2026 Devaluation

Last updated on

If you're looking at alternatives already, here's what you should definitely read before moving to the next tab.

Table of Content

The Indian credit card world just hit a massive speed bump recently. On February 26, 2026, SBI Card dropped a notice that about a massive devaluation that that effectively "killed" the most loved card in India: the SBI Cashback Credit Card.

For a long time, this card was the "GOAT" (Greatest of All Time). If you were smart with your money, you had this card. Now, the community is in shock.

Here's exactly what changed with SBI Cashback card, why it happened, and which card you should think of as a solid alternative.

Anatomy of the SBI Cashback Card Devaluation: Dissecting the March 2026 Notice

The changes, officially published on February 26, 2026, and slated to take effect on April 1, 2026, represent a multi-pronged restriction on how value is generated, tracked, and extracted from the SBI Cashback Credit Card. This is not a mere tweaking of rates; it is a fundamental restructuring of the card's unit economics, designed to halt revenue leakage and discourage gamified spending.

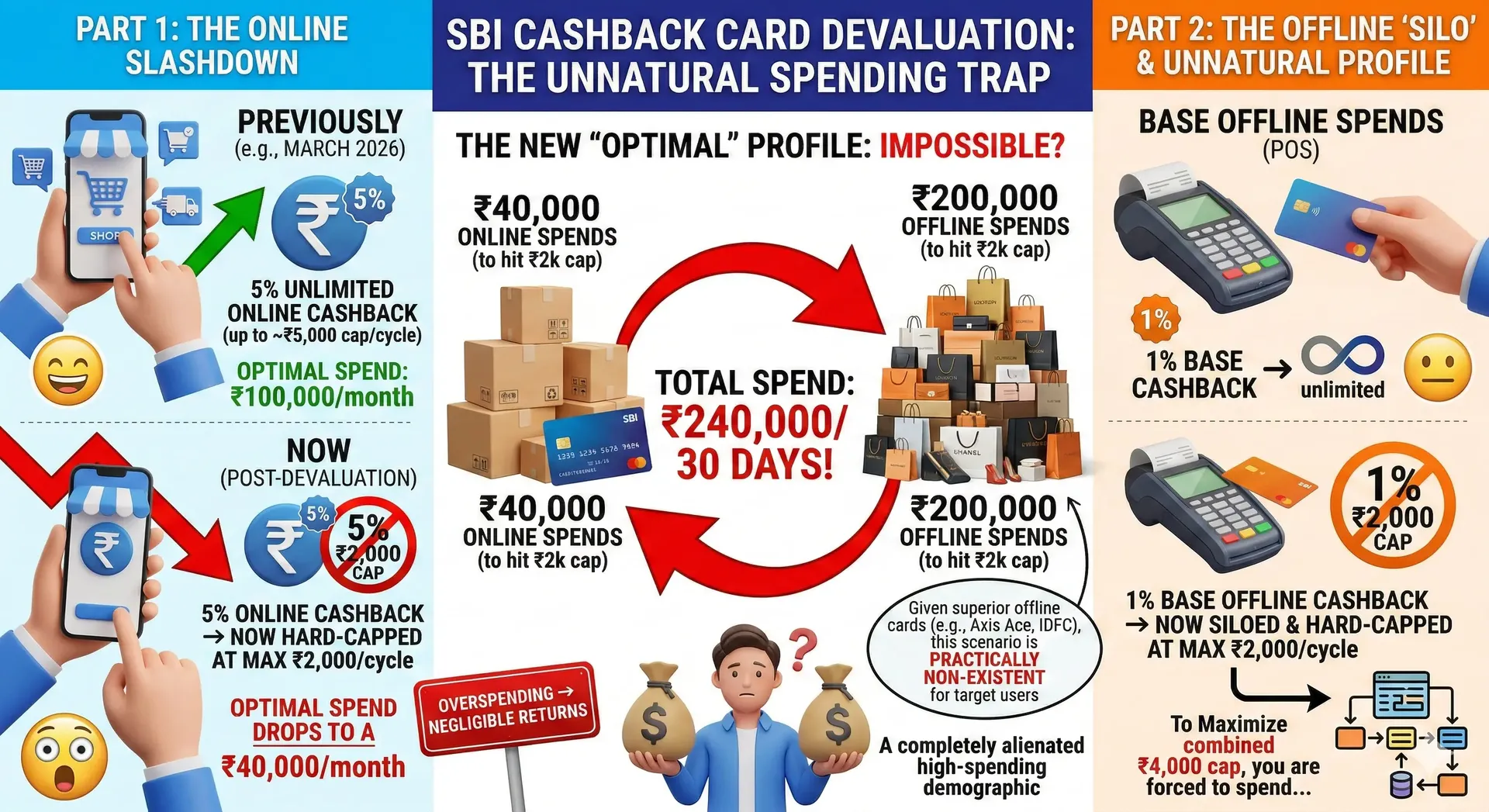

Historically, the SBI Cashback Credit Card dominated the Indian market by offering a simple, flat 5% cashback on virtually all online spending, governed by a highly generous cap of ₹5,000 per statement cycle. This allowed cardholders to spend up to ₹100,000 per month through digital channels while continuously earning the accelerated 5% rate, outperforming even the most elite super-premium credit cards in the country.

Under the new regime, the architecture of the card has been dismantled and rebuilt with aggressive restrictions.

The most catastrophic change is the severe reduction in the cashback ceiling. The maximum cashback a cardholder can earn within a single statement cycle has been slashed by 20% to ₹4,000, but the true damage lies in the bifurcation of this limit.

The 5% cashback on online spends is now subjected to a hard cap of maximum ₹2,000 per statement cycle. As a result, the optimal spending threshold for online purchases drops precipitously from ₹100,000 to a mere ₹40,000 per month. Any online expenditure exceeding ₹40,000 in a billing cycle will effectively yield negligible returns under the accelerated category, completely alienating the high-spending demographic that initially championed the product.

Simultaneously, the 1% base cashback, typically accrued on offline point-of-sale (POS) transactions at merchant outlets, has also been siloed and capped at a maximum of ₹2,000 per statement cycle.7

In addition to the caps, SBI Card has weaponized its Merchant Category Code (MCC) policy, aggressively expanding its list of excluded categories to surgically remove high-volume, low-margin transaction types that optimizers frequently exploited for points arbitrage.

Also Read: All Changes to SBI Cashback Credit Card [Including Excluded MCC and Revised Terms

Alternatives to SBI Cashback Card: Creating a Post-Devaluation Card Portfolio

With the SBI Cashback card effectively dethroned for individuals routing more than ₹40,000 through online channels monthly, what card should you have in your wallet.

Well, it seems the time of 'one-card-does-all' seems to be ending. Now, everyone wanting to optimize for spends must focus on a multi-card setup where distinct cards are deployed for highly specific transaction categories.

Here are your available options as of March 2026 which I am continuously evaluating.

1. Bank of Baroda (BOBCARD) Cashback Credit Card: The New SBI Cashback Card Rival

Quietly launched in the latter half of the previous year by BOBCARD, a wholly-owned subsidiary of Bank of Baroda, this card has rapidly ascended the ranks to position itself as the most direct, aggressive competitor to the diminishing SBI offering. It is engineered specifically to capture the displaced, moderately high-spending online consumer by providing a highly transparent, value-driven experience centered on direct statement credits.

The BOBCARD operates on an attractive "Happy Returns" concept. Unlike traditional cards that force users through a convoluted portal to redeem points at varying, opaque conversion ratios, the BOBCARD focuses on an automated, direct cashback model.

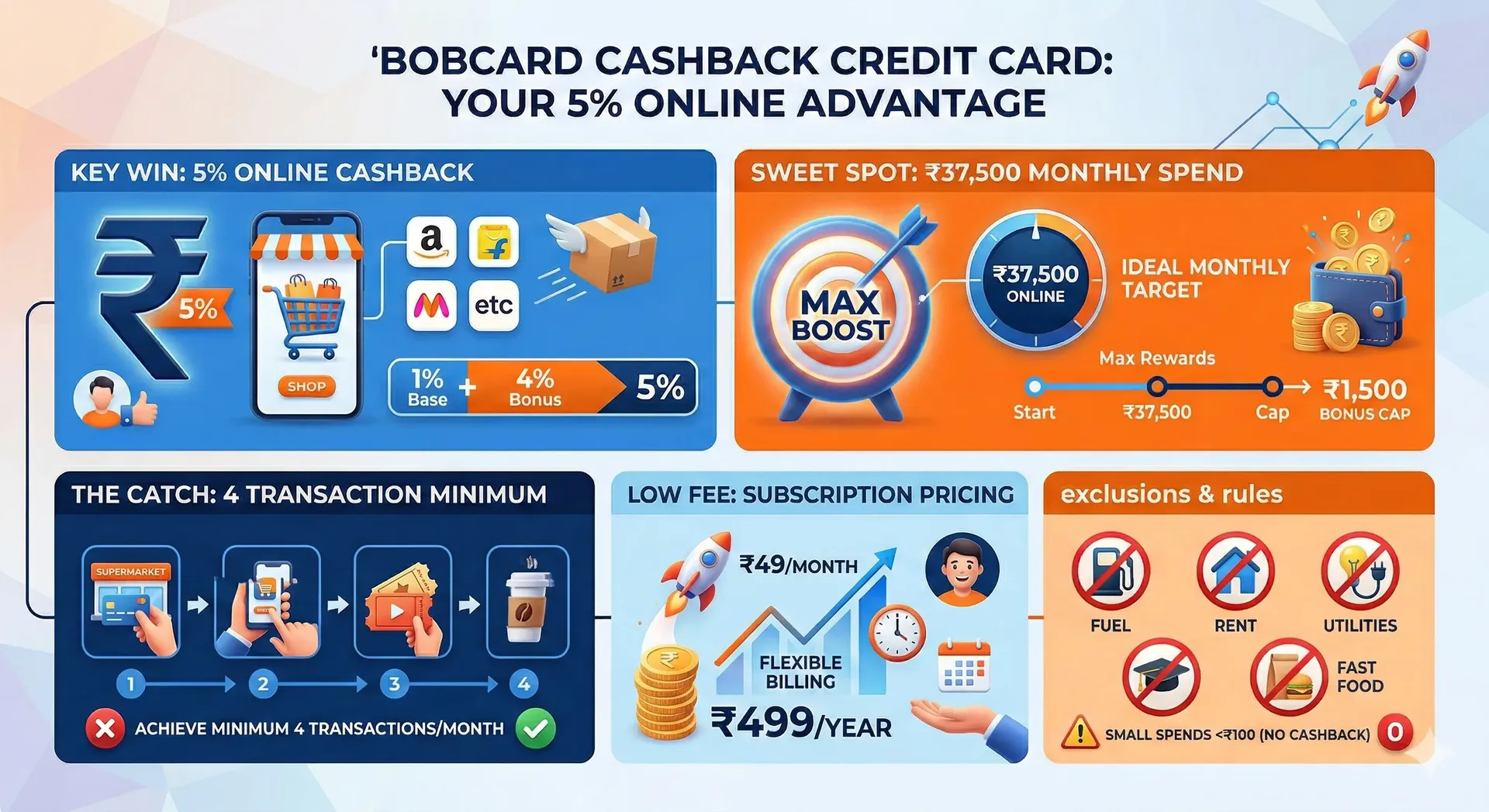

- The Big Win: You get 5% cashback on all domestic online shopping. This is split as 1% base + 4% bonus.

- The "Sweet Spot": The bonus cashback is capped at ₹1,500. To max this out perfectly, you should spend ₹37,500 per month online.

- No Point Hassle: It uses a "Happy Returns" model, meaning the cashback hits your statement directly. No hunting through portals to redeem points.

- Subscription Pricing: Instead of one big yearly fee, you pay ₹49/month (about ₹499/year), which is half the cost of the SBI card.

- The "Catch": You must make at least 4 separate transactions in a month to unlock the 5% rate.

- Small Spends Don't Count: Anything under ₹100 earns zero cashback.

- The Standard Exclusions: No rewards on the usual suspects: Fuel, Rent, Utilities, Education, Government services, and (surprisingly) Fast Food.

My analysis told me that to maximizes the accelerated cashback tier, you must precisely spend ₹37,500 per month online. This threshold sits remarkably close to SBI's newly minted ₹40,000 limit, making the BOBCARD an almost perfect, seamless replacement for users whose online expenditures naturally fall within this bandwidth.

Furthermore, the card provides a standard 1% base cashback rate on eligible domestic offline transactions and all international transactions, ensuring a baseline return on physical swiping.

However, the BOBCARD is not without its own specific friction points and engineered hurdles.

- To qualify for the accelerated 4% cashback in any given billing cycle, the cardholder is mandated to execute a minimum of 4 distinct transactions. This prevents users from simply making one large ₹37,500 purchase and abandoning the card for the rest of the month.

- Furthermore, micro-transactions below ₹100 are explicitly excluded from accruing any cashback whatsoever, effectively eliminating value from small, daily convenience purchases.

- The card also carries an extensive exclusion list that rigorously mirrors current industry standards; expenditures on Fuel, Rent, Utilities, Education, Government services, Supermarkets, Wallets, Charity, and Fast Food restaurants are all entirely ineligible for rewards.

From a cost perspective, the BOBCARD features a unique, modern subscription-style billing model. Cardholders are charged ₹49 per month, equating to an annualized fee of ₹499.

Given this significantly lower acquisition and holding cost compared to SBI's ₹999 fee, the BOBCARD presents a highly efficient, mathematically superior alternative for the entry-to-mid-level spender whose online lifestyle expenditures hover securely around the ₹30,000 to ₹35,000 mark.

2. HDFC Swiggy Credit Card: Fit for Urban Lifestyle

As generalized cashback caps tighten, specialized co-branded cards seem like a good option, too. If your spends are majorly for food delivery, quick-commerce, etc, the HDFC Swiggy Credit Card can work.

The card's primary and most aggressive draw is a massive 10% cashback across the entire, expansive Swiggy ecosystem. This includes standard restaurant food ordering, Swiggy Instamart, Swiggy Dineout (restaurant bill payments), and Swiggy Genie (hyper-local package deliveries).

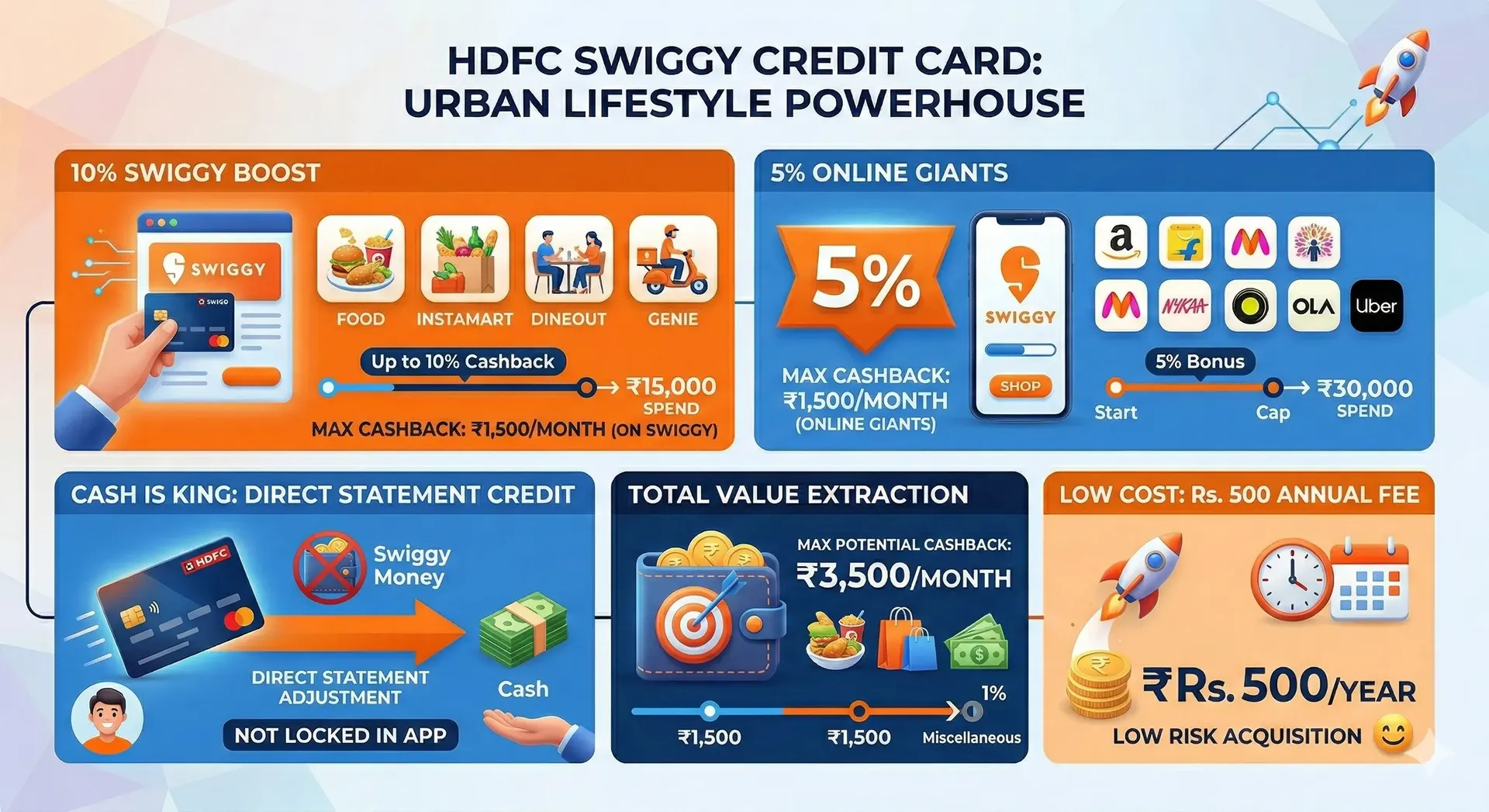

- The 10% Swiggy Benefit: You get 10% cashback on everything inside the Swiggy app: Food, Instamart (groceries), Dineout (restaurant bills), and Genie. This is capped at ₹1,500 per month.

- The 5% "Online" Bonus: You also get 5% cashback on other big platforms like Amazon, Flipkart, Myntra, Nykaa, Ola, and Uber. This has its own separate ₹1,500 monthly cap. You maximize this cashback by spending ₹30,000 on these sites.

- Amazing Recent Update: A huge update recently changed how you get paid. Instead of getting "Swiggy Money" that you can only spend back in the app, the cashback is now credited directly to your credit card statement as real money.

- Low Cost, High Reward: The annual fee is just ₹500.

At a highly accessible annual fee of Rs. 500, the card is a low-risk acquisition. However, the total potential value extraction across all categories is strictly hard-capped at an absolute maximum of ₹3,500 per month.

For a user whose lifestyle naturally aligns with the Swiggy platform and who also maintains moderate general online shopping habits, this card easily outpaces the newly devalued SBI Cashback card in total absolute value, provided they are willing to track their category-specific spending caps diligently.

3. HSBC Live+ Credit Card: The Realistic Offline Companion Card

The devaluation of sweeping online cards has exposed a significant blind spot in many consumer portfolios: physical, offline expenditures. To bridge this gap, the HSBC Live+ Credit Card started giving more benefits for offline lifestyle, dining, and grocery expenditures, capturing immense value from mandatory household spending that historically generated negligible returns.

- The 10% "Essentials" Bonus: You get a 10% cashback on dining, food delivery (Swiggy/Zomato), and groceries (both online and physical supermarkets). It’s capped at ₹1,000 per month, which you hit perfectly by spending ₹10,000: a very realistic budget for most households.

- The Unlimited 1.5% Safety Net: This is the card's secret weapon. For everything else (electronics, medical bills, retail), you get an unlimited 1.5% cashback. This beats the standard 1% offered by almost every other card in the market.

- Zero-Fee Potential: The annual fee is ₹999, but it gets completely waived if you spend ₹2 Lakhs in a year.

- Travel & Dining Perks: You get 4 free domestic lounge visits per year (one per quarter) and a 15% discount at partner restaurants through their dining program.

- Usage Strategy: It’s the perfect "partner card." Use it for your mandatory household expenses that other flashy cards usually ignore.

While the cap appears low, maximizing it requires only a highly realistic ₹10,000 in monthly grocery or dining spend: a figure that represents the baseline food budget for most urban families.

Plus, for all other un-categorized expenditures, the card provides a highly competitive 1.5% base cashback rate that is entirely unlimited.

This effectively acts as a robust safety net for large, miscellaneous purchases (such as electronics, medical bills, or general retail) that fall outside specialized bonus categories, significantly outperforming the standard 1% base rate offered by almost all direct competitors.

It has rapidly become an essential secondary or tertiary card in a post-devaluation portfolio, quietly capturing massive value on the mundane, mandatory household expenditures that flashier cards ignore.

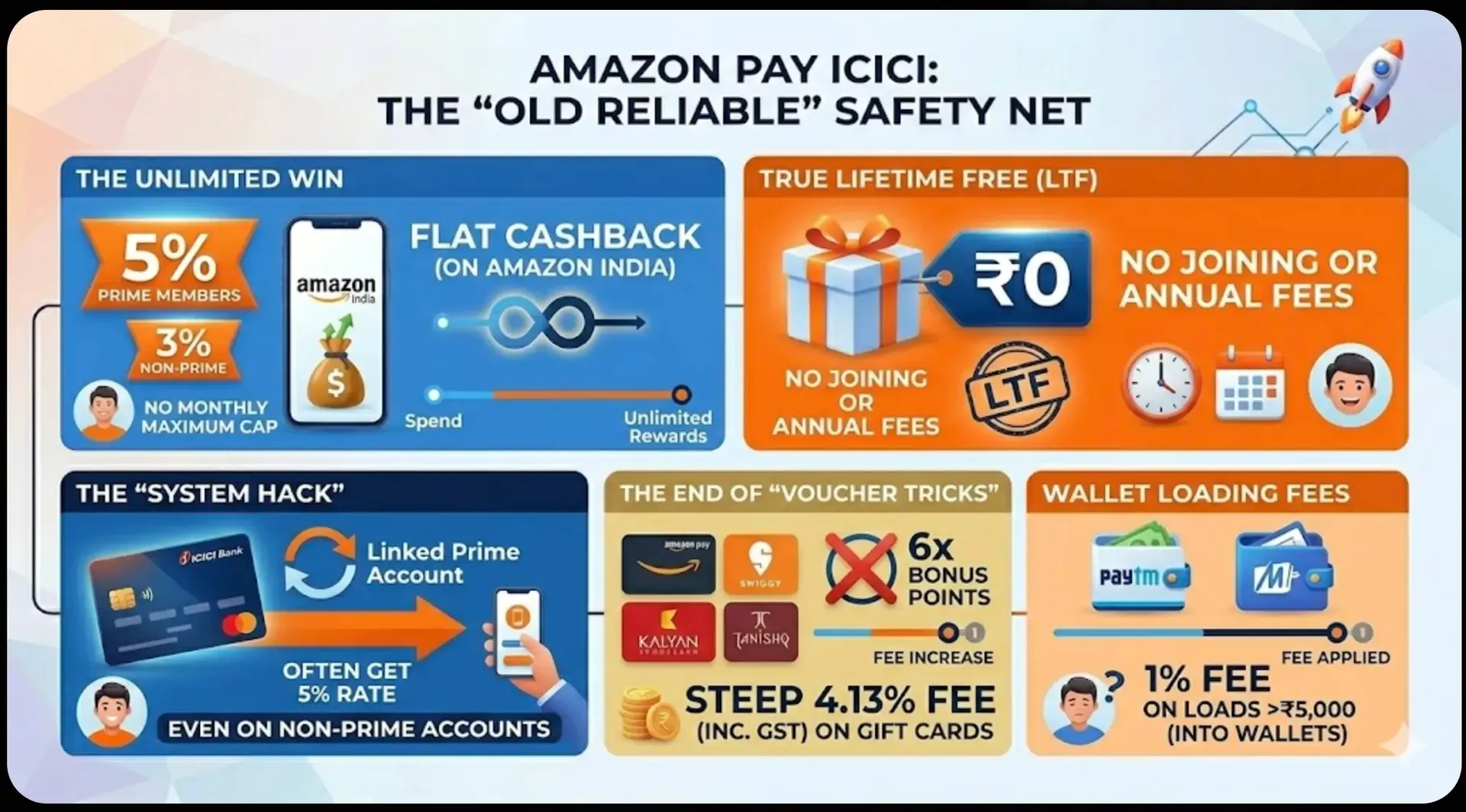

4. Amazon Pay ICICI Bank Credit Card: The Online Companion

Having over 5 million active customers, this solid credit card remains a bedrock product despite weathering its own series of recent, peripheral devaluations.

The core value proposition of the card remains untouched and unparalleled: it offers a flat, reliable 5% unlimited cashback on Amazon India purchases for Amazon Prime members, and a 3% unlimited return for non-Prime members. The true, defining power of this card lies precisely in its lack of a monthly maximum cap and its lifetime free (LTF) status.

It costs nothing to hold and can safely process massive, unlimited volumes of e-commerce spending without needing to check a remaining quota.

- The Unlimited Win: You get a flat 5% cashback on Amazon (for Prime members) or 3% (for non-Prime). The best part? There is no monthly cap.

- True Lifetime Free (LTF): There are no joining fees or annual charges. It costs you ₹0 to keep this card in your drawer forever.

- The Verdict: It is still the king for buying things directly on Amazon, but it's no longer a good tool for paying utilities through "backdoor" voucher tricks.

The card has not been entirely immune to the industry-wide era of rationalization. While the core Amazon spend is totally secure, ICICI Bank has aggressively devalued the card's utility in sophisticated arbitrage and manufactured spending scenarios. Effective early 2026, the bank surgically removed the highly lucrative 6x accelerated reward points that were previously available when purchasing iShop vouchers for commonly used brands like Amazon Pay, Swiggy, Kalyan Jewellers, and Tanishq.

Furthermore, ICICI Bank attacked the economics of gift card arbitrage. They increased the processing fees on voucher purchases (including Flipkart, Swiggy, and Amazon Shopping vouchers) to a steep 3.5% plus GST, resulting in an effective fee of 4.13%—up from the previous 2.95% or 0% structures.

While other cards are busy adding complicated caps and hidden rules, the Amazon Pay ICICI card remains the simplest "defensive" card in your wallet. It’s the card you use when you want to buy big-ticket electronics or appliance where other card cashback limits would hit.

SBI Cashback Card Alternatives 2026: Comparative Analysis

To effectively navigate this fragmented landscape, consumers must transition from viewing credit cards in isolation to analyzing them as interconnected components of a holistic financial strategy. The table below provides a concise, structured comparison of the newly established market hierarchy.

Credit Card | Annual Fee (₹) | Primary Accelerated Cashback | Strict Monthly Cap on Accelerated Category | Base Rate / Un-categorized | Optimal Target Demographic / Deployment Strategy |

SBI Cashback (Post-April '26) | 999 | 5% General Online | ₹2,000 | 1% (Now capped at ₹2,000) | Moderate, generalized online shoppers whose total digital spend strictly stays below ₹40,000/month. |

BOBCARD Cashback | 499 (or 49/mo) | 5% Domestic Online | ₹1,500 | 1% | Budget-conscious, diversified online shoppers capping at ₹37,500/month; an entry-level SBI replacement. |

HDFC Swiggy | 500 | 10% Swiggy Ecosystem; 5% Online | ₹1,500 (Swiggy); ₹1,500 (General Online) | 1% (Capped at ₹500) | Urban professionals heavily reliant on food delivery and quick-commerce; requires active limit tracking. |

HSBC Live+ | 999 | 10% Offline Dining & Physical Groceries | ₹1,000 | 1.5% (Completely Unlimited) | Household managers prioritizing offline grocery shopping and dining out; excellent base rate safety net. |

Amazon Pay ICICI | Nil (Lifetime Free) | 5% Amazon India (Requires Prime) | Unlimited | 1% | High-volume Amazon loyalists; the ultimate defensive card for unlimited, un-capped major appliance or tech purchases. |

FAQs: SBI Card Devaluation & What to Do Next

1. When do the new SBI Cashback rules actually start?

The changes take effect on April 1, 2026. Any spending you do before this date will still fall under the old rules (5% back up to ₹5,000). If you have big purchases planned, it’s best to get them done before the April deadline.

2. Is the SBI Cashback card still worth the ₹999 annual fee?

It depends on your spending. If you spend exactly ₹40,000 online every month, you still earn ₹2,000 back. Over a year, that’s ₹24,000 in cashback, which easily covers the fee. However, if you regularly spend over ₹50k–₹60k online, you’re leaving a lot of money on the table and should look at a secondary card.

3. What happens if I spend more than ₹40,000 online in a month?

Once you hit the ₹2,000 cashback cap (which happens at ₹40,000 of spending), your rewards drop to zero for any further online purchases in that billing cycle. You won't even get the 1% base rate for online spends once the cap is reached.

4. Can I still get rewards for paying my taxes or utility bills?

Sadly, no. SBI has specifically added Government Services, Tolls, and Digital Gaming to their list of exclusions. Most other banks are following suit, so your best bet for these categories now is to use specific "Utility" focused cards.

5. Which card is the best "seamless" replacement for SBI?

The BOBCARD Cashback is the most direct rival. It offers the same 5% online cashback rate and has a monthly cap that is very similar (₹1,500). If you want to keep your "one-card" lifestyle as close to the original as possible, this is the winner.

About the Author

Anmol

Anmol writes detailed blogs and content about credit cards available in India and how to take full advantage of credit cards while avoiding marketing noise.