How to Pay Your Debt When You Owe a Bank, an App, and Your Family (and Which One)?

Last updated on

Owe a bank, a loan app and family all at once? Skip the one-size answer. Use this matrix and calculator to split your surplus the smart way.

Too busy to read endless reviews & research?

Find the best cards that suit your lifestyle in 30 seconds

Try Monzy NowNo signup or email required

You owe three different people, and each one pulls at you differently.

The bank doesn't ask, it just auto-debits your EMI on the 5th, and if the balance isn't there, it charges a penalty and dents your CIBIL score. The loan app does the same, but keeps harassing you through calls.

Your uncle, the one who lent you money for a family emergency two years ago, says "no rush, beta" every time you meet, and somehow that "no rush" sits heavier every time you meet at a family gathering, than any recovery agent's call.

So which one do you clear first?

TL; DR: The Quick Answer

Protect your CIBIL first (never miss a formal EMI). Start a small emergency buffer in parallel. Then attack the most expensive legitimate, active debt, usually a credit card or loan app at 40%+ a year. Keep interest-free family debt moving steadily, not fast. And a disputed or already-overpaid predatory loan doesn't get prioritised, it gets resolved. The calculator below does this math for your exact mix.

If you type that into Google, you'll get a one-word answer: avalanche. Pay the highest-interest debt first. It's good advice. It's also incomplete, because it was written for someone who owes a credit card company and a car loan, not someone who owes a bank, an app, and a person they meet every now and then.

But your life has variables most ‘standard’ frameworks ignore. Remember the following if you’re in a similar situation:

- If it's all family and friends, no interest, no urgency: breathe. You're not in a fire. Build your buffer first, then pay everyone steadily in proportion. Speed isn't the goal, showing up every month is.

- If you're carrying a credit card or an active loan app at 40%+: that's the emergency, even if it's the smallest balance. Protect your EMIs, keep a token buffer forming, and pour everything else onto that toxic debt until it's gone. Don't invest a rupee until it is.

- If you're stuck in between, some family debt, some formal EMIs, maybe one nasty app loan: follow the order above, and let the calculator do the splitting. The one thing you should never do is try to fight all of them at full speed at once. That's how people burn out and give up in month three.

Remember, whatever your mix: debt repayment is a marathon, not a 100-metre race.

Warikoo worked through a similar situation in a recent Money Matters episode.

The person: 22 years old, ₹28,000 in-hand, about ₹11,000 in living costs, so roughly ₹17,000 spare each month.

He owed ₹3,00,000 to three relatives (interest-free, borrowed for a family wedding, no urgency) plus a ₹50,000 loan-app balance that had ballooned from ₹30,000, that he'd already paid nearly ₹45,000 toward, and was disputing.

The naïve avalanche move says: the app loan is the "highest cost," so throw all ₹17,000 at it. Wrong call here. He'd already overpaid it, it was under dispute, and emptying his surplus into it would leave zero buffer, so the next emergency becomes the next app loan.

Warikoo's split:

₹5,000 into an emergency buffer, ₹12,000 to the family loan, divided the way the three lenders had lent it. At ₹12,000 a month, ₹3,00,000 clears in 25 months, even with zero salary growth. The disputed loan gets resolved on its own track, not fed. And one sharp instruction that most people miss: don't raise that ₹12,000 later, even when you can afford to. With patient lenders, steady on-time repayment is what buys their peace, not speed.

Watch out for three traps.

- "Interest-free" family debt isn't actually free: the cost is the relationship. But that's exactly why consistency beats speed. A steady ₹12,000 every month buys more goodwill than an unpredictable ₹20,000-then-nothing.

- Don't deprioritise a legitimate, active 40%+ loan just because it "feels informal." The rule keys on legal status, not vibes. An active loan-app balance you genuinely owe is toxic debt, attack it like a credit card.

- Never drain your buffer to zero to finish faster. That's the exact move that sends people back to borrowing. Slower-but-protected beats faster-but-fragile every time.

The two debt repayment methods everyone quotes (and what they actually mean)

If you’ve watched standard repayment advice on YouTube, or read about the ways to repay, there are two ways to attack multiple debts.

Both are real, both work. But which one is for you?

- The avalanche method means you pay the minimum on everything, then throw every spare rupee at the debt with the highest interest rate, regardless of how big or small it is. You kill the most expensive one, then move to the next-most-expensive. It saves you the most money, full stop, because you're starving the debt that grows fastest.

- The snowball method means you ignore interest rates and attack the smallest balance first. You clear one debt quickly, feel the win, and use that momentum on the next. It costs you slightly more in interest, but for a lot of people, seeing one loan actually disappear is the thing that keeps them going.

The avalanche usually wins. And there’s a reason for that. Let me illustrate with an example.

Say you've got a ₹50,000 credit card balance at roughly 42% a year, that's the reducing-balance rate most cards in India charge, where interest is calculated on what you still owe, not the original amount.

On ₹50,000, that's around ₹1,750 a month just in interest, before you've paid off a single rupee of the actual balance.

A ₹1,00,000 personal loan at 14% costs you about ₹1,170 a month in interest, on double the balance. The card is the smaller loan but the bigger fire.

Avalanche says: put out the fire, not the loan that merely looks scarier.

So far, textbook approach. But now the part, you’re here for: What should you do if you’re in debt from multiple sources?

A variable most ‘imported advice’ debt repayment misses

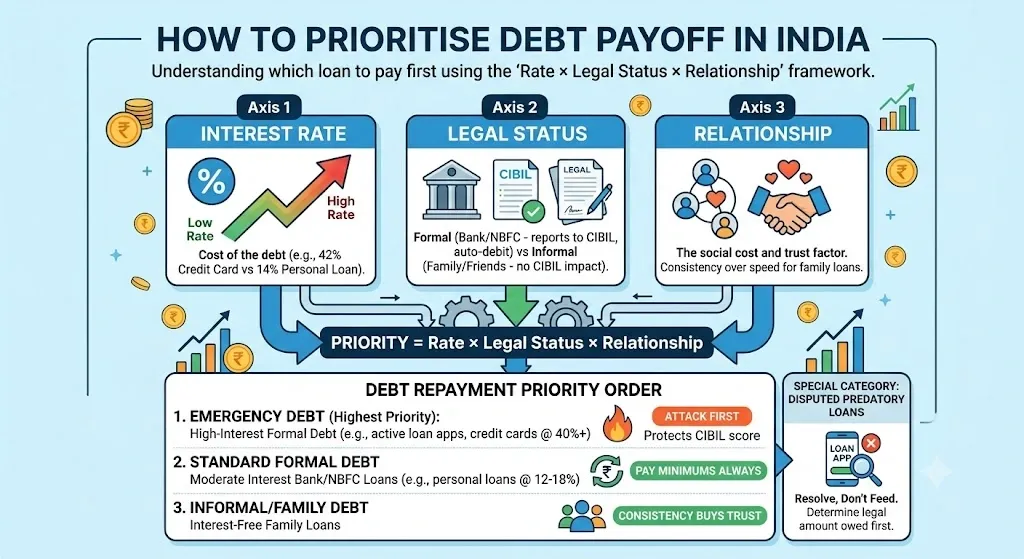

Interest rate tells you about the cost of the debt. But it misses that here, in India, it’s more than the costs.

People avail different kinds of debts, simultaneously. And they all behave differently (and have different implications):

- Formal debt: From a bank or NBFC (a non-banking finance company, the regulated lenders behind most personal loans). It is contractual, auto-debits EMIs, reports to CIBIL, and a single missed EMI can stay on your credit report for up to 7 years. Basically, this debt has long-term implications.

- Informal debt. Taken from family or a friend, usually carries no paperwork, and no CIBIL impact. But it carries a different kind of cost, one no calculator prices in: the quiet weight on a relationship you can't refinance.

- Predatory debt. Taken from an unregulated loan app where a ₹30,000 loan somehow becomes ₹50,000, is its own category. These are the worst kinds that can leave you in debt traps. And if you’re stuck with predatory loans (and have paid in excess), the smartest move can be to dispute.

Put all these together in a single life situation, and you get a simple rule that's far more useful than "highest rate first":

Priority = interest rate × legal status × relationship.

- A debt that's expensive, formal, and legitimate gets attacked hard.

- A debt that's informal, and personal gets paid steadily, because with family, consistency is the currency, not speed.

- And a debt that's inflated, unregulated, and disputed gets resolved before it gets fed.

Your Action Plan for Repayment (If You’re in a Similar Situation)

- Cover every formal EMI's minimum, on time, without fail. It's important to protect your CIBIL score, which gets you cheaper loans, a decent credit card, etc. One missed EMI can undo months of progress. This comes before everything.

- Start a small emergency buffer if you have surplus. This feels wrong when you're in debt. Protection comes before speed. Without a buffer, the next time your phone screen cracks or a medical bill lands, you reach for another loan app, and you're back where you started, except deeper. A boring, liquid buffer is the wall that stops the cycle.

- Now attack the most expensive legitimate, active debt. Usually that's a credit card or an active loan-app balance at 40%+ a year. This is the same avalanche method, and here it's exactly right, no investment reliably beats a guaranteed 42% saving.

- Keep interest-free family debt moving steadily. Ideally in the proportion each person lent, so no one feels skipped. Don't maximise this at the cost of steps 1–3. You're not buying speed here; you're buying trust, and trust is bought with a predictable amount arriving every month, not a heroic lump sum once.

- A disputed or overpaid predatory loan doesn't get "prioritised”. If a ₹30,000 loan ballooned to ₹50,000 and you've already paid most of it, pouring more money into a claim you're contesting is throwing good money after bad. Figure out what's legal and what you genuinely owe first.

Frequently Asked Questions about Debt Repayment in India

Should I pay off the highest-interest loan or the smallest one first?

On pure cost, highest-interest first (the avalanche method) always saves you more money. Choose smallest-first (snowball) only if you've tried before and lost motivation, the quick win of clearing one loan can be what keeps you going. For most people, avalanche is the right call.

Should I pay off a family loan or a bank loan first?

Usually the bank loan, because it charges interest and reports to your CIBIL, missing it costs you money and your credit score. But keep the family loan visibly moving in parallel, because the "interest" you pay there is trust, and it compounds too.

Is it worth paying off an interest-free loan early?

There's no cost reason to rush it, the money isn't growing. But there's a relationship reason to keep it steady and predictable. Pay a consistent amount every month rather than clearing it in one dramatic go and starving your other priorities.

Should I stop my SIP to clear debt?

If the debt is charging 40%+ a year, yes, pause investing and clear it first. No mutual fund reliably returns 40%, so every rupee you put into an SIP instead of that debt is a rupee losing the race. Keep a small emergency buffer, kill the toxic debt, then restart investing.

Can I settle a loan for less to close it faster?

Be careful. When a lender marks a loan "settled" rather than "closed," it flags on your CIBIL report as a partial default and can hurt you for years. And never borrow from a second app to pay off the first — that's the exact trap that doubles people's debt.

You've got a clearer picture now than most people who are drowning in this ever get. Put your numbers in, pick your order, and start. Month one is the hard one, after that, it's just showing up.

Disclaimer: This is my honest read, not formal financial advice. I'm not your advisor, and before you act on anything big, run it past a professional who knows your full situation. But this is exactly how I'd think about it if these were my debts.

About the Author

Anmol Ratan Sachdeva

Anmol has been tracking the Indian credit card market since 2019, reviewing benefits, changes across 40)+ cards and documenting issuer devaluations in real time. He personally has a card portfolio across HDFC, Axis, SBI Card, ICICI, and writes from direct usage experience. His analysis focuses on real-world return calculations rather than headline reward rates. He writes content for educational purposes.